Ontem, ao chegar a casa, tinha finalmente à minha espera o último livro de Rita Mcgrath, "The End of Competitive Advantage".

.

Já não sei porquê, há dias tirei da estante um livro que li durante a primeira metade da década de 90 do século passado, "A Gestão em Tempo de Mudança" de Tom Peters, no original "Thriving on Chaos".

.

Na primeira página pode ler-se:

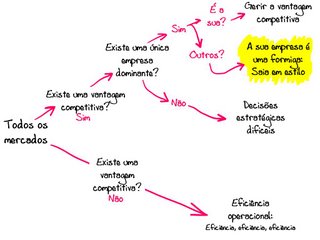

"Nenhuma empresa está em segurança. (Moi ici: Perigosa propaganda neoliberal, dirão uns). Em 1987, e no futuro previsível, não existe aquilo a que se poderá chamar um avanço "sólido", ou até substancial, em relação à concorrência. Existem grandes mudanças para que alguém possa ser complacente. Além disso, os ciclos de "vencedor a vencido" vão-se tornando cada vez mais curtos."

Já não me lembrava de ter lido isto... isto já faz parte de mim.

.

Quando comecei a ler este livro de Tom Peters era, literalmente, operário da indústria química, fazia turnos na nova unidade de produção de PVC da CIRES em Estarreja. Li estas coisas e esqueci-as... não me esqueci delas, esqueci-me de as ter lido. Assim, elas deixaram de ser algo exterior a mim e passaram a fazer parte de mim, moldaram o meu pensamento e influenciam-no até hoje.

.

Já na altura tinha a mania de sublinhar os livros:

Em 1987 os EUA viviam os efeitos do choque das exportações japonesas. Penso que já aqui fiz no blogue, por mais de uma vez, o paralelismo entre as exportações japonesas e a economia americana dos anos 80 do século passado e a nossa economia da primeira década do século XXI e as exportações chinesas.

.

Tom Peters na página sublinhada compara dois mundos, o mundo que era e é e o mundo que deverá ser. Reparem no que ele escreveu em 1987:

"Era/É

Mercados de massas, publicidade para as massas...

Deverá ser

Criação especialmente de nichos de mercado, inovação em termos de aproximação aos mercados, aproveitamento da fragmentação do mercado, constante diferenciação de todos os produtos (por muito implantados que estejam)"

.

Interessante pensar como Tom Peters estava muito à frente... e perceber como isto me influenciou. Li, esqueci-me que li mas algures em 2005 ou 2006 saiu-me cá de dentro como meu, como a resposta para explicar e enquadrar os sintomas que via a contrariar os profetas da desgraça.

%2006.21.jpeg)