.

Chris Anderson escreveu o livro "A Cauda Longa", recordo que foi com ele que comecei a usar a metáfora "Mongo".

.

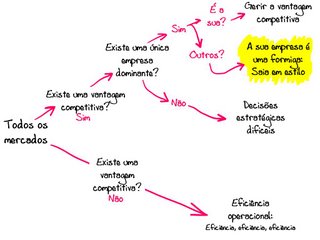

O que significa para uma PME trabalhar para a cauda longa?

Significa trabalhar para nichos e tirar partido da profundidade da relação com cada cliente, em vez de vender para a massa de clientes e tirar partida da escala.

.

E o que acontece a quem trabalha para nichos mas não tem a cadeia de valor alinhada nesse propósito?

.

Aprendi com Verónica Martinez:

- "Cuidado com a ISO 9001" (03/2007)

- "Atenção à gestão da cadeia de valor" (07/2009)

- "Alinhamento na cadeia de fornecimento" (04/2013)

Quem trabalha para nichos mas não tem a cadeia de valor alinhada nesse propósito vai ter problemas.

.

Os fornecedores de matérias-primas e acessórios vão dar preferência aos clientes que lhes dão mais a ganhar. Por isso, as encomendas para as pequenas quantidades que vão para os produtos dos nichos são guardadas para o fim, são entregues muito mais tarde. Ao serem entregues mais tarde vão rebentar com todos os compromissos de entrega para os nichos.

.

Muitas empresas que trabalham para nichos fazem-no em simultâneo com o trabalho para outros grupos mais volumosos. O interesse dos nichos são as margens superiores que geram; contudo, as empresas não querem abdicar das quantidades que o volume dá. Assim, elas próprias também não estão optimizadas, ora produzem lotes maiores, ora produzem lotes com quantidade 1.

.

E não se definem porque em boa verdade não têm uma estratégia.

.

São empresas que têm a cauda longa dentro de si.

.

São empresas que têm a cauda longa dentro de si.