Em 1996 Slywotzky escreveu sobre a "Value Migration".

.

Em 2003 Michael J. Silverstein e Neil Fiske com John Butman escreveram "Trading Up - Why Consumers Want New Luxury Goods - and How Companies Create Them" (BTW, este livro, lido recentemente na diagonal impressiona pela forma como descreve o modelo de vida baseado na casa como máquina ATM)

.

Em 2005 The McKinsey Quarterly publicou o excelente "The vanishing middle market"

.

Em 2006 Michael Silverstein escreveu "Treasure Hunt" onde o autor fala da polarização do mercado, chama-lhe "The Bifurcating Market" e se concentra no fenómeno do Trading-Down (julgo que seria útil para a Centromarca o seu estudo).

.

A situação económica em países como Portugal, Espanha, Irlanda, Grécia e Estados Unidos, vão ampliar ainda mais as oportunidades de negócio para quem, actuando no mercado interno, se dirige para os clientes que valorizam o preço (daí que não veja com grande expectativa este movimento "Empresas à descoberta do mercado nacional", eventuais sucessos serão sempre marginais).

.

O José Silva é radical e defende "A Amazonização do comércio é inevitável. O comércio de B2C em mercados, super, hiper ou lojas foram criados no tempo pré-internet. Hoje já não se justificam, nem as respectivas marcas de comércio"

.

Pessoalmente, ainda acredito em marcas de comércio e ainda acredito em lojas físicas. No entanto, talvez os conceitos de marca e de loja tenham de evoluir para algo de diferente.

.

Mas em linha com o pensamento do José Silva, esta entrevista sobre o modelo de negócio da não-organização "The Rise of Unorganizations".

.

Já conheci várias não-organizações, o seu grande trunfo era a rapidez e a flexibilidade, mas não passavam pela internet... outros tempos.

A apresentar mensagens correspondentes à consulta middle-market ordenadas por relevância. Ordenar por data Mostrar todas as mensagens

A apresentar mensagens correspondentes à consulta middle-market ordenadas por relevância. Ordenar por data Mostrar todas as mensagens

terça-feira, março 08, 2011

segunda-feira, novembro 12, 2018

"Uber", Mongo e a educação (parte II)

Parte I.

Mais uma peça para a construção de uma reflexão sobre o futuro da educação em Mongo em "Young Americans need to be taught skills, not handed credentials":

_-_Google_Art_Project_-_edited.jpg/1280px-Pieter_Bruegel_the_Elder_-_The_Tower_of_Babel_(Vienna)_-_Google_Art_Project_-_edited.jpg)

Mais uma peça para a construção de uma reflexão sobre o futuro da educação em Mongo em "Young Americans need to be taught skills, not handed credentials":

"One recent survey found that 43 per cent of college grads are underemployed.Voltaremos ao século XIX? A escola pública existe para servir os funcionários,

.

This certainly mirrors what I hear from chief executives, many of whom tell me they cannot find the skills they need either at the top or the bottom of the socio-economic ladder. Ivy League colleges are great for those who can afford them but most education has become completely disconnected from the needs of both students and the labour market.

.

There are plenty of MBAs who can read a balance sheet but have neither operational nor soft skills. Four-year business administration graduates are settling for low wage gigs, while $20-an-hour manufacturing jobs go unfilled because employers can’t find anyone with vocational training.

.

Desperate companies are trying to plug the gap — telecoms group AT&T has set up an internal online course to train the 95 per cent of those in its own technology and services unit that have inadequate ability in Stem subjects — Science, Technology, Engineering and Maths. Walmart Academy has trained thousands of workers, including in basic skills they should have learnt in high schools.

...

Perhaps the most successful and scalable bridging of the skills and credentials gap thus far has been the P-Tech high school, initially started by IBM as a way to create a middle-market talent pool and now said to run with 500 other industry partners in 110 schools in eight states."

2/2 voltaremos a ver a genuína escola comercial oliveira martins no porto, suportada pelo sector e independente do ministério da educação?— Carlos P da Cruz (@ccz1) October 6, 2015

"Então, veio-me à mente a conversa deste mês de Agosto com estudante da FCUP do curso de Ciências de Computação. Segundo ele, o curso foi objecto de reformulação há dois anos. No entanto, continua a não dar toda uma série de linguagens de programação que as empresas precisam mas que os professores não dominam, nem têm motivação para aprender (esse estudante passou parte do mês de Agosto a estudar programação para Android nos cursos da Udacity).Daqui, de onde também recordo:

.

Se a FCUP optasse por contratar professores para darem aulas sobre essas linguagens os professores incumbentes sofreriam."

"Há uma frase feita qualquer acerca das organizações que se aplica como uma luva neste caso:

Quando a velocidade da mudança no exterior, no contexto, no entorno de uma organização, é muito maior que a velocidade a que essa organização consegue mudar... temos outra Torre de Babel:"

domingo, outubro 23, 2016

Acerca da importância da clareza

"we identify two types of companies with purpose. The first type, high purpose-camaraderie organizations, includes companies that score high on purpose and also on dimensions of workplace camaraderie (e.g. “This is a fun place to work”; “We are all in this together”; “There is a family or team feeling here”). The second type includes high Purpose-Clarity organizations that score high on purpose but also on dimensions of management clarity (e.g. “Management makes its expectations clear”; “Management has a clear view of where the organization is going and how to get there”).Não basta um bom ambiente, é também preciso clareza sobre qual o destino e como vamos lá chegar.

.

When we replaced our initial measure of purpose with these measures capturing the two types of purpose organizations, we found that only the high Purpose-Clarity organizations exhibit superior accounting and stock market performance."

.

E vale a pena sublinhar o papel das chefias intermédias:

"We also found that middle managers and professional workers seem to be the key players in driving this relationship, not hourly workers and not top executives. This last finding underscores the absolute importance of fostering an effective middle manager layer within firms: managers who buy into the vision of the company and can make daily decisions that guide the firm in the right direction.Trechos retirados de "The Type of Purpose That Makes Companies More Profitable"

.

Ultimately, our study suggests that purpose does, in fact, matter. But it only matters if it is implemented in conjunction with clear, concise direction from top management and in such a way that the middle layer within the firm is fully bought in."

quinta-feira, maio 04, 2017

Para reflexão

"Only about 1.1% of the world population is German. However, 48% of the mid-sized world market leaders come from Germany.[Moi ici: A tríade acha que isto só acontece por causa de um marco fraco. Tolos!]Recordar este texto "Empresas pequenas concentradas em nichos mundiais"

...

But the reasons they are a predominantly German phenomenon are many. This includes the German history of many small independent states (until 1918 Germany consisted of 23 monarchies and three republics), which forced entrepreneurs to internationalize early on in a company’s development if they wanted to keep growing. [Moi ici: Aprender a fazer o by-pass aos Estados, um conselho deste blogue desde 2007] In addition, there are traditional regional crafts, such as the clock-making industry in the Black Forest with its highly developed fine mechanical competencies, which developed into 450 medical technology companies, most of them makers of surgical instruments.

...

A further pillar of the Hidden Champions’ competitive strength is the unique German dual system of apprenticeship, [Moi ici: Algo que enfrentou forte oposição dos proto-geringonços] which combines practical and theoretical training in non-academic trades. The Hidden Champions invest 50% more in vocational training than the average German company.

.

Tax advantages are another reason. The high taxes on assets in France and the inheritance tax in the U.S. prevent the accumulation of capital necessary for the formation of a strong mid-sized sector. [Moi ici: Como diz a filha do assaltante de bancos, "Temos de perder a vergonha de ir buscar a quem está a acumular dinheiro"]

"Assim, temos empresas concentradas em servir um nicho, por isso é que eu os achei (aos alemães) tão arrogantes no meu primeiro encontro profissional... os pedidos da minha empresa estavam a desviar-se do nicho onde eles nadavam... um nicho é, por definição, pequeno. Se uma empresa se mantém concentrada num nicho e quer crescer só há um caminho... percorrer o mundo à procura de mais clientes que se encaixem no nicho... a geografia tem de ser irrelevante para eles."E comparar:

"Why is this mental internationalization so important? Because while Hidden Champions may be small, they compete on a global scale. They achieve world-class quality by keeping their focus narrow; focus is the most important element of a Hidden Champion’s strategy. Flexi, for example, makes only one product — retractable dog leashes — but has the claim to make them better than anyone else. This has allowed them to reach 70% of market share in this category. But focus makes a market small. How can you make it bigger? By globalizing."

Trechos retirados de "Why Germany Still Has So Many Middle-Class Manufacturing Jobs"

quinta-feira, fevereiro 26, 2009

Re-pensar, reflectir sobre o que resulta e continuará a resultar

Se o pântano traiçoeiro do middle-market se está a alargar na sequência da migração de valor em curso, talvez faça sentido re-pensar o que sempre se fez.

.

Será que é adequado continuar a usar os mecanismos de promoção do passado?

.

A promoção das marcas é mais importante do que nunca, por isso faz todo o sentido olhar para o exemplo dos excêntricos que vão à frente, talvez se possa aprender com as suas experiências.

.

Assim, a revista The Economist publica o artigo "A new look - Creative destruction meets haute couture".

.

Alguns trechos:

.

"This season many designers chose to abandon the catwalk, the very symbol of fashion.

...

some designers ... decided to cut costs by holding smaller spectaculars at their own showrooms. Others opted for even thriftier “presentations”, where models were hired to stand on podiums like mannequins for a few hours, or to mingle with the ordinary mortals in the crowd.

.

The collections were also smaller, a sign of the reduced demand for luxury clothing. Department stores have already said they will curb buying, reining in designers who used to make the same dress in a dozen hues.

...

a popular French designer, has spent the past three months reworking her website to make it more “human and interactive”. Fashion, she points out, was historically sold through intimate salons. She wants to re-establish that accessibility—and the internet allows her, and others, to do it cheaply."

.

No Público de hoje, na mesma onda, o artigo "Crise já chegou às feiras organizadas pela Exponor":

.

"O número de expositores e visitantes das feiras da Exponor, em Matosinhos, está a diminuir "10 a 15 por cento" devido ao clima de crise, disse à agência Lusa fonte do parque de exposições. "O clima recessivo está a ter efeitos nas feiras. Há empresas que estão a fechar e outras que deixam de vir às feiras","

,

Todos têm de reflectir, quer os expositores, quer os organizadores dos eventos.

.

Será que é adequado continuar a usar os mecanismos de promoção do passado?

.

A promoção das marcas é mais importante do que nunca, por isso faz todo o sentido olhar para o exemplo dos excêntricos que vão à frente, talvez se possa aprender com as suas experiências.

.

Assim, a revista The Economist publica o artigo "A new look - Creative destruction meets haute couture".

.

Alguns trechos:

.

"This season many designers chose to abandon the catwalk, the very symbol of fashion.

...

some designers ... decided to cut costs by holding smaller spectaculars at their own showrooms. Others opted for even thriftier “presentations”, where models were hired to stand on podiums like mannequins for a few hours, or to mingle with the ordinary mortals in the crowd.

.

The collections were also smaller, a sign of the reduced demand for luxury clothing. Department stores have already said they will curb buying, reining in designers who used to make the same dress in a dozen hues.

...

a popular French designer, has spent the past three months reworking her website to make it more “human and interactive”. Fashion, she points out, was historically sold through intimate salons. She wants to re-establish that accessibility—and the internet allows her, and others, to do it cheaply."

.

No Público de hoje, na mesma onda, o artigo "Crise já chegou às feiras organizadas pela Exponor":

.

"O número de expositores e visitantes das feiras da Exponor, em Matosinhos, está a diminuir "10 a 15 por cento" devido ao clima de crise, disse à agência Lusa fonte do parque de exposições. "O clima recessivo está a ter efeitos nas feiras. Há empresas que estão a fechar e outras que deixam de vir às feiras","

,

Todos têm de reflectir, quer os expositores, quer os organizadores dos eventos.

quinta-feira, setembro 17, 2015

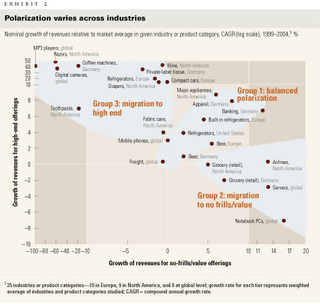

Polarização balanceada

Recupero a figura que se segue, do artigo "The Vanishing Middle Market" que referi em "Porque não podemos ser uma Arca de Noé! (II)"

E chamo a atenção para o Grupo 1: onde se verifica a polarização mercado (crescimento simultâneo do premium e do low-cost, com o desaparecimento do meio-termo). No Grupo 1 está a cerveja na Europa e na Alemanha.

E chamo a atenção para o Grupo 1: onde se verifica a polarização mercado (crescimento simultâneo do premium e do low-cost, com o desaparecimento do meio-termo). No Grupo 1 está a cerveja na Europa e na Alemanha.

.

Por um lado assistimos à explosão da cerveja artesanal. Os números são impressivos. Ver: "THE YEAR IN BEER: 2014 CRAFT BEER IN REVIEW FROM THE BREWERS ASSOCIATION" (Gostei sobretudo desta demonstração de Mongo:

.

Por um lado assistimos à explosão da cerveja artesanal. Os números são impressivos. Ver: "THE YEAR IN BEER: 2014 CRAFT BEER IN REVIEW FROM THE BREWERS ASSOCIATION" (Gostei sobretudo desta demonstração de Mongo:

"Craft beer appreciators are becoming as diverse as craft beer itself."Por outro lado, assistimos a esta consolidação das consolidações:

- "Cervejas: SABMiller estará disponível para uma oferta potencial da AB InBev";

- "Dona da Budweiser quer rival e controlar metade dos lucros da indústria cervejeira"

quinta-feira, fevereiro 12, 2015

A polarização dos mercados já vem de longe

Na senda de “The vanishing middle market” (Maio de 2006) e do fenómeno da polarização dos mercados, "How a Two-Tier Economy Is Reshaping the U.S. Marketplace":

.....

E, já agora, "Rushing to Cater to America’s Rich"

.....

E, já agora, "Rushing to Cater to America’s Rich"

quarta-feira, julho 10, 2013

Curiosidade do dia

"The explosive growth of China’s emerging middle class has brought sweeping economic change and social transformation—and it’s not over yet. By 2022, our research suggests, more than 75 percent of China’s urban consumers will earn 60,000 to 229,000 renminbi ($9,000 to $34,000) a year.

.

In purchasing-power-parity terms, that range is between the average income of Brazil and Italy. Just 4 percent of urban Chinese households were within it in 2000—but 68 percent were in 2012. In the decade ahead, the middle class’s continued expansion will be powered by labor-market and policy initiatives that push wages up, financial reforms that stimulate employment and income growth, and the rising role of private enterprise, which should encourage productivity and help more income accrue to households. Should all this play out as expected, urban-household income will at least double by 2022."

Para desmaquilhar alguns mitos.

.

Trecho retirado de "Mapping China’s middle class"

terça-feira, janeiro 26, 2016

Pricing man (parte II) - para reflexão

Mais um trecho retirado de "Confessions of the Pricing Man: How Price Affects Everything" de Hermann Simon.

"Countries show significant differences in how profitable their companies are. I have tracked data on this topic for many years, and attribute some of the results to cultural norms. Figure 5.1 compares the average profit margins for companies in 22 countries.US companies are in the middle of the pack at 6.2 %. German companies have an average after-tax profit of 4.2 %, placing them in the lower half despite their improved performance in the recent past. Japanese companies have assumed their customary place near the bottom, with a meager 2.0 %. The average across all countries works out to 6.0 %..What causes these sharp differences? To a large degree it is a matter of having the wrong goals. While I wouldn’t say these numbers are completely self-fulfilling prophecies, they do reflect the priorities that companies set. Too many companies have given higher priority to goals other than profit....There is nothing inherently wrong with having sales, volume, and market share targets. Most companies have them and work hard to strike the right balance. These three secondary goals, however, offer you no useful guidance for price setting. Price setting requires a thorough understanding of two things: how your customers perceive your value and the profit level you need to sustain or improve that value. If market share is your primary goal, why don’t you just give away your product for free? Or even pay customers to use it? Of course such a strategy makes no sense. The reality in almost all companies is that goal setting is not an “either-or” exercise..Balance is paramount. The central problem is that most companies are not balanced. They still underemphasize profits relative to such goals as market share, revenue, volume, or growth. And they misunderstand the often dire consequences of that prioritization. This imbalance results in bizarre pricing strategies and ineffective marketing tactics."

quinta-feira, setembro 06, 2012

Working to raise prices

Há dois tipos de empresas, as que trabalham para subir os preços e as que trabalham para reduzir os custos.

.

Só exagerando um pouco, pode dizer-se que só há 2 segmentos disponíveis: vender cada vez mais caro, com maior valor acrescentado potencial e; vender com custos cada vez mais baixos, sendo muito eficiente. É o fenómeno da bipolarização identificado pela expressão: polarização do mercado.

.

A primeira vez que li sobre o fenómeno foi em 2005, num artigo que me impressionou e ficou na memória, "The vanishing middle market", citado, por exemplo, neste postal com o mesmo nome. Por exemplo, esta notícia de hoje "o segmento automóvel que mais está a sofrer é o da gama média, enquanto os de luxo baixaram as vendas, mas não na mesma extensão" enquadra-se neste fenómeno que é pré-crise, a crise apenas o potenciou.

.

Trabalhar para reduzir os custos é um desafio honesto e, por vezes, o rumo correcto a seguir. No entanto, não é para quem quer, é para quem pode.

.

No entanto, para muitas empresas que querem ser bem sucedidas na exportação, o que defendo e proponho é exactamente o oposto, o trabalhar para subir os preços.

.

Este blogue está cheio de recomendações e sugestões acerca deste desafio, por exemplo, só nesta semana:

Por tudo isto, é agradável ler e perceber:

"Sapatos portugueses já são os segundos mais caros do mundo"

(Gráfico retirado daqui.)

.

E, no entanto, apesar dessa subida de preços:

"Em termos estratégicos, o mercado alemão é uma espécie de “desígnio” sectorial. Com efeito, a economia germânica continua a revelar-se como o principal impulsionador da Zona Euro e é igualmente o mercado europeu onde as importações de calçado mais estão a crescer. Acresce que Portugal colocou na Alemanha, no primeiro semestre, 5,3 milhões de pares de calçado no valor de 148 milhões de euros, o que representa um acréscimo de 8,5% relativamente ao mesmo período do ano anterior. (Moi ici: E quanto é que cresceu a economia alemã?) Razão de sobra para uma grande investida do calçado português à «feira das feiras» de Dusseldorf."E, no entanto:

"Fora do espaço europeu, franco destaque para os importantes crescimentos nos EUA (mais 60 por cento para 9 milhões de euros), Rússia (mais 31 por cento para 8,7 milhões de euros), Angola (43 por cento para 6,3 milhões de euros), Japão (mais 30 por cento para 6,2 milhões de euros) e Canadá (5,1 por cento para 5,3 milhões de euros)"E o que é que previa a academia para o sector?

quarta-feira, abril 30, 2014

um sintoma de que doença(s)?

Durante mais uma caminhada, tive oportunidade de ler este relatório da consultora Roland Berger "Escaping the commodity trap – How to regain a competitive edge in commodity markets". Um tema e um desafio que tratamos, há vários anos, quer neste blogue quer no dia-a-dia profissional.

.

Caricaturando, posso pensar que os clientes-tipo da consultora ou são Golias ou aspiram a ser Golias, por isso, dão muita ênfase ao que podem controlar e crescer é o fim e não uma consequência. Por isso, estão cada vez mais afastados dos clientes e pensam que o logotipo da marca aguenta tudo... não aguenta, porque num mundo onde a assimetria de informação a favor da empresa está cada vez mais ameaçada, o valor durante o uso é cada vez mais fácil de percepcionar antes da compra.

"A "commodity trap" describes a situation where even complex products and services are downgraded to "commodities", with limited differentiation and where competition is primarily price-based – this is due to a combination of developments experienced by customers, competitors and in products/technologiesNo final a consultora apresenta 5 factores-chave para o sucesso no combate à armadilha da comoditização:

.

The commodity trap is a phenomenon found in all industries – over 60% of the study participants have been affected, 54% have yet to take sufficient action to escape (and among affected companies even 65%). At many companies, there is a significant gap between recognizing the commodity trap and reacting accordingly [Moi ici: Quem são os clientes de uma consultora como a Roland Berger? Qual será a tipologia das empresas que fazem parte do universo questionado?].

In most industries, commoditization already started some 5 years ago – almost all industries report their low-end market segments as being affected, [Moi ici: Algo perfeitamente expectável, já o que se segue começou por me chocar...] more than half of the participants also see their middle segments being hit and about 20% face commoditization even in their premium segments." [Moi ici: O que significa isto? Isto é um sintoma de que doença(s)? Como não fazer a ponte para esta interrogação do Paulo Peres "Marcas serão mais vulneráveis no futuro?" ou para aquela que parece ser a ideia-base do livro que tenho na lista para ler "Absolute Value: What Really Influences Customers in the Age of (Nearly) Perfect Information" de Itamar Simonsen and e Emanual Rosen. Faz algum sentido uma oferta premium estar comoditizada? Não é um sintoma de um profundo distanciamento entre clientes e marcas?]

"1 Core competencies – Leverage core competencies to develop new know-how or business opportunitiesPorque acredito no Estranhistão, porque acredito que cada vez mais "We are all weird" [and proud of it], porque acredito no mundo de tribos apaixonadas, fico surpreendido pela pouca ênfase colocada na cada vez maior importância da escolha dos clientes-alvo, na cada vez maior importância da interacção.

.

2 Thinking outside the box – Look beyond the current business model for ways out of the commodity trap

.

3 Change management – Be aware that successful implementation, especially for business model innovations, requires comprehensive change management actions

.

4 Value chain & market segments – Analyze all directions along the value chain and potential market segments in order to find the "white spot" for your future business

.

5 Sustainability – Think of long-term, sustainable ways to escape a commodity trap – short-term actions usually only postpone the problem"

.

Caricaturando, posso pensar que os clientes-tipo da consultora ou são Golias ou aspiram a ser Golias, por isso, dão muita ênfase ao que podem controlar e crescer é o fim e não uma consequência. Por isso, estão cada vez mais afastados dos clientes e pensam que o logotipo da marca aguenta tudo... não aguenta, porque num mundo onde a assimetria de informação a favor da empresa está cada vez mais ameaçada, o valor durante o uso é cada vez mais fácil de percepcionar antes da compra.

sexta-feira, dezembro 06, 2013

Duas economias

Este artigo "Increasing Returns and the New World of Business" parece-me que de certa forma ilustra o problema dos membros da tríade.

.

Os membros da tríade foram educados na economia e nos modelos e "leis" da economia de Magnitograd, de Metropolis, do século XX e, da produção em massa de commodities. Entretanto, estamos a caminho do Estranhistão onde a economia é outra:

.

Os membros da tríade foram educados na economia e nos modelos e "leis" da economia de Magnitograd, de Metropolis, do século XX e, da produção em massa de commodities. Entretanto, estamos a caminho do Estranhistão onde a economia é outra:

"Marshall’s world of the 1880s and 1890s was one of bulk production: of metal ores, aniline dyes, pig iron, coal, lumber, heavy chemicals, soybeans, coffee - commodities heavy on resources, light on know-how. In that world it was reasonable to suppose, for example, that if a coffee plantation expanded production it would ultimately be driven to use land less suitable for coffee—it would run into diminishing returns.

...

Marshall said such a market was in perfect competition, and the economic world he envisaged fitted beautifully with the Victorian values of his time. It was at equilibrium and therefore orderly, predictable and therefore amenable to scientific analysis, stable and therefore safe, slow to change and therefore continuous. Not too rushed, not too profitable. In a word, mannerly. In a word, genteel.

.

With a few changes, Marshall’s world lives on a century later within that part of the modern economy still devoted to bulk processing: of grains, livestock, heavy chemicals, metals and ores, foodstuffs, retail goods—the part where operations are largely repetitive day to day or week to week. Product differentiation and brand names now mean that a few companies rather than many

compete in a given market. But typically, if these companies try to expand, they run into some limitation: in numbers of consumers who prefer their brand, in regional demand, in access to raw materials. So no company can corner the market. And because such products are normally substitutable for one another, something like a standard price emerges. Margins are thin and nobody makes a killing. This isn’t exactly Marshall’s perfect competition, but it approximates it.

...

Because the two worlds of business—processing bulk goods, and crafting knowledge into products - differ in their underlying economics, it follows that they differ in their character of competition and their culture of management. It is a mistake to think that whatworks in one world is appropriate for the other.

...

Let us look at the two cultures of competition. In bulk processing, a set of standard prices typically emerges. Production tends to be repetitive—much the same from day to day or even from year to year. Competing therefore means keeping product flowing, trying to improve quality, getting costs down. There is an art to this sort of management, one widely discussed in the literature. It favors an environment free of surprises or glitches—an environment characterized by control and planning.

...

Competition is different in knowledge-based industries, because the economics are different. ... Hierarchies flatten not because democracy is suddenly bestowed on the work force or because computers can cut out much of middle management. They flatten because, to be effective, the deliverers of the next-thing-for-thecompany need to be organized like commando units in small teams that report directly to the CEO or to the board."

quarta-feira, fevereiro 25, 2009

O desafio

No DN de hoje: "Marcas brancas representam já um terço das compras"

.

"Os portugueses estão a comprar cada vez mais produtos das marcas próprias dos supermercados. Em 2008, estes artigos representaram 32% das vendas totais, registando um crescimento em valor de 21% em relação ao ano anterior, segundo dados da TNS Worldpanel

.

As marcas próprias (brancas) dos supermercados estão a ganhar terreno com a crise. Em 2008, estes artigos registaram um crescimento em valor de 21% face ao ano anterior. Segundo dados da TNS Worldpanel, estes produtos representam já 32% das vendas de artigos de grande consumo. Do lado contrário, as marcas de fabricantes registaram uma queda de 3%.

.

O preço é, assim, um dos principais factores que os portugueses têm em conta quando fazem as suas compras."

.

Julgo que podemos conciliar estes factos com com a migração de valor em curso.

.

Julgo, igualmente que podemos conciliar estes factos com as palavras de Kjell Nordstrom no Público de hoje no artigo "A inovação e a emoção vão resistir à crise" assinado por Ana Rita Faria:

.

"Numa crise como a actual, fazer o mesmo que todos os outros fazem é uma má ideia. Ninguém quer pagar mais por uma cópia ou por algo que se parece como outra coisa qualquer.

.

Mas será que as empresas vão arriscar e inovar? Não será mais seguro continuar a imitar?

.

Quem o fizer está a cair numa armadilha. Claro que é mais barato e conveniente copiar do que inovar. Mas, em contrapartida, acaba por ser ainda mais arriscado porque a empresa se coloca a si mesma numa situação em que, mais tarde ou mais cedo, vai perder. Crises como a actual mostram que realmente temos de fazer as coisas de um modo diferente." (Daí o meu sublinhado para aquelo trecho "as marcas de fabricantes registaram uma queda de 3%")

.

"Que tipo de companhias vão sobreviver à crise?

Há dois tipos: as grandes multinacionais como a Siemens, ou as pequenas empresas especializadas como a Apple. No fundo, serão as companhias inovadoras e que, simultaneamente, têm uma relação muito próxima com o consumidor e são capazes de o seduzir."

.

IMHO responderia:

.

No fundo serão as companhias inovadoras, nos seus processos de fabrico e logística (para o negócio do preço-baixo) e as que se viram para o exterior e apostam na sedução do consumidor (para o negócio da marca).

.

Se não for através da sedução do consumidor como é que as marcas dos fabricantes vão conseguir espaço na prateleira da distribuição? Quando a distribuição também tem as suas marcas (brancas ou próprias)?

.

ADENDA (9h00): Durante o meu jogging matinal reflecti mais um pouco sobre o que está em causa.

.

A crise em curso, em boa verdade, não veio trazer novos factores ao cenário.

A crise em curso apenas veio exacerbar as forças, as correntes que já estavam em curso e alterar as fronteiras do meio-termo.

A crise em curso veio alargar as fronteiras do que é o meio-termo pantanoso e traiçoeiro.

A crise em curso veio reforçar a polarização do mercado que já estava em curso, basta recordar The vanishing middle-market.

.

"Os portugueses estão a comprar cada vez mais produtos das marcas próprias dos supermercados. Em 2008, estes artigos representaram 32% das vendas totais, registando um crescimento em valor de 21% em relação ao ano anterior, segundo dados da TNS Worldpanel

.

As marcas próprias (brancas) dos supermercados estão a ganhar terreno com a crise. Em 2008, estes artigos registaram um crescimento em valor de 21% face ao ano anterior. Segundo dados da TNS Worldpanel, estes produtos representam já 32% das vendas de artigos de grande consumo. Do lado contrário, as marcas de fabricantes registaram uma queda de 3%.

.

O preço é, assim, um dos principais factores que os portugueses têm em conta quando fazem as suas compras."

.

Julgo que podemos conciliar estes factos com com a migração de valor em curso.

.

Julgo, igualmente que podemos conciliar estes factos com as palavras de Kjell Nordstrom no Público de hoje no artigo "A inovação e a emoção vão resistir à crise" assinado por Ana Rita Faria:

.

"Numa crise como a actual, fazer o mesmo que todos os outros fazem é uma má ideia. Ninguém quer pagar mais por uma cópia ou por algo que se parece como outra coisa qualquer.

.

Mas será que as empresas vão arriscar e inovar? Não será mais seguro continuar a imitar?

.

Quem o fizer está a cair numa armadilha. Claro que é mais barato e conveniente copiar do que inovar. Mas, em contrapartida, acaba por ser ainda mais arriscado porque a empresa se coloca a si mesma numa situação em que, mais tarde ou mais cedo, vai perder. Crises como a actual mostram que realmente temos de fazer as coisas de um modo diferente." (Daí o meu sublinhado para aquelo trecho "as marcas de fabricantes registaram uma queda de 3%")

.

"Que tipo de companhias vão sobreviver à crise?

Há dois tipos: as grandes multinacionais como a Siemens, ou as pequenas empresas especializadas como a Apple. No fundo, serão as companhias inovadoras e que, simultaneamente, têm uma relação muito próxima com o consumidor e são capazes de o seduzir."

.

IMHO responderia:

.

No fundo serão as companhias inovadoras, nos seus processos de fabrico e logística (para o negócio do preço-baixo) e as que se viram para o exterior e apostam na sedução do consumidor (para o negócio da marca).

.

Se não for através da sedução do consumidor como é que as marcas dos fabricantes vão conseguir espaço na prateleira da distribuição? Quando a distribuição também tem as suas marcas (brancas ou próprias)?

.

ADENDA (9h00): Durante o meu jogging matinal reflecti mais um pouco sobre o que está em causa.

.

A crise em curso, em boa verdade, não veio trazer novos factores ao cenário.

A crise em curso apenas veio exacerbar as forças, as correntes que já estavam em curso e alterar as fronteiras do meio-termo.

A crise em curso veio alargar as fronteiras do que é o meio-termo pantanoso e traiçoeiro.

A crise em curso veio reforçar a polarização do mercado que já estava em curso, basta recordar The vanishing middle-market.

segunda-feira, fevereiro 01, 2016

O mundo a mudar, outra vez (parte I)

O mundo a mudar, outra vez, "German Exporters Shudder as China Economy Slows":

.

Já reparou como a China se está a transformar numa economia de consumo?

E que impacte terá esta evolução na economia alemã? Quais as consequências para o resto da eurozona?

E que impacte terá esta evolução na economia alemã? Quais as consequências para o resto da eurozona?

"German exports to the important Chinese market are suffering their sharpest drop in a quarter of a century, casting a shadow over Europe’s biggest economy and showing the global impact of China’s slowdown.

.Que oportunidades e ameaças para a sua PME por trás desta evolução?

With new orders from China and other emerging economies sagging, German businesses fear the bad news is only beginning, data and surveys released in recent days suggest.

.

German exports to the U.S. and many other markets are still growing, cushioning the impact of China’s troubles. But with much of Europe still licking its wounds from the long eurozone debt crisis, business confidence in Germany is vulnerable to continued cooling in Asia.

...

Above all, capital-goods sales to Chinese factories are down, as overcapacity there takes its toll on investment spending.

...

The stakes are high for Germany. The 30 companies in its DAX stock-market index have 672 subsidiaries in China, according to the Munich-based consultancy EAC.

...

Some Chinese companies have started to dump unused machinery on the market, further hurting German companies’ sales and profit margins.

.

Bright spots remain. Many German companies in consumer and service sectors say they’re benefiting from China’s rapidly growing middle class. Engineering companies that can help China improve its infrastructure and relieve traffic pressures, and environmental-technology companies whose equipment can help reduce pollution, are also reporting growing orders.

...

But it is the U.S. that is doing most to compensate for China’s stumble. German exports to the U.S. rose just over 19% from January to November from a year earlier, according to the statistics office."

.

Já reparou como a China se está a transformar numa economia de consumo?

sexta-feira, maio 22, 2015

"how prices are framed and the context of the purchase significantly influence our willingness to pay"

"When economists were treating preference, price, and value as stable and absolute, Kahneman, Tversky, and other psychologists argued that in the human mind, everything is relative and depends on context. And when we say everything we really mean everything, from judgments of physical attractiveness to judgments of reference, price, and value. Almost all human judgments are made in relation to a reference point.

...

“Our perception of, and reaction to, reality is subjective. How you feel about products, or even about your life, is at least as important, and probably much more important, than the product or your life’s objective characteristics.”

...

the brain didn’t evolve to perceive reality as it is. It evolved to make approximations that are reliable.

...

Coherent arbitrariness tells us that absolute preferences are volatile, but relative preferences are stable. This creates an illusion of order that disguises the largely arbitrary nature of how we value things.

...

If we accept coherent arbitrariness, we should dismiss (or at least discourage) the idea that market price is solely determined by a balance between demand and supply. [Moi ici: Ehehehe subversão para cima da tríade] Just like the valuation of the man’s wealth depends on his wife’s sister’s husband, his willingness to pay for a product depends on his perception of fairness, not a cold calculation of what the product should be worth based on its market price. The behavioral economist would argue that even though market price is not entirely arbitrary - no one could get away with selling a six-pack of beer for one thousand dollars - how prices are framed and the context of the purchase significantly influence our willingness to pay.

...

The second interpretation is that high and low anchors make us feel like we’re deciding rationally, even though we’re probably just responding to social pressures and loss aversion—we don’t want to be perceived as cheap, but we don’t want to get ripped off, so we opt for the middle option.

...

in the luxury trade where expensive items that don’t sell change what does. Thus, if a retailer wants to sell a pair of shoes that cost $100, they should put them next to a pair of shoes that cost $150. That way, the retailer will activate the trade-off contrast principle, which says that if item X is clearly better than item Y consumers will tend to buy X, even when X is only better relative to Y—and potentially worse than comparable items.[Moi ici: Recordar o exemplo das conservas da Comur]

.

Neoclassical economic models predict that customers weigh all the options rationally. In reality, when we encounter too much choice - just like we would in a shoe store - we tend to opt for items that we can justify. We talk ourselves into X because it looks better than Y."

Deliciosos trechos retirados de "What Makes Us Tick?"

quinta-feira, dezembro 29, 2016

"Midsize companies can’t compete ... on scale"

"Companies with between $10 million and $1 billion in sales saw 6.3 percent revenue growth in first quarter 2016, compared to just 1.1 percent for the economy as a whole, according to the National Center for the Middle Market.Trechos retirados de "How midmarket companies use tech to compete with the big guys"

...

Differentiation is key.

Midsize companies can’t compete with their large-cap counterparts on scale, so they need other ways to differentiate themselves. One way to do that, said Bala Ganesh, senior director of marketing for the US 2020 Team at UPS, is to offer a unique customer experience. “Just purely competing on price is impossible for smaller retailers,” Ganesh said. “You want to create unique products, a unique experience or some unique bundle not available from big box retailers.”.

One example might be to build a social community of like-minded consumers around a product offering, where the price of admission is a purchase or service subscription. [Moi ici: Uma tribo] Or bundle existing products and services in customized ways [Moi ici: Fugir do vómito industrial que só pensa em uniformidade] not available from larger outlets. “This is how they can hit above their average,” Ganesh added.

.

Ganesh identifies five areas where midmarket companies must excel to play in the big leagues: product selection, a flawless web or mobile experience, shipping and delivery transparency, flexible pickup options and an easy return process. “This is what drives demand. The consumer buying journey doesn’t end after you click buy, and more and more retailers are recognizing that,” Bala said."

sábado, janeiro 17, 2009

Este é o tempo para repensar a estratégia (parte XI)

Ainda há dias escrevi neste postal The vanishing middle market:

.

"Esta crise talvez não tenha criado nada de realmente novo no mundo dos negócios!

...

Talvez esta crise em que estamos mergulhados a nível mundial não tenha feito mais do que acelerar algo que já estava em curso."

.

Entretanto, o The McKinsey Quarterly publica uma entrevista (A fresh look at strategy under uncertainty: An interview) com Hugh Courtney, autor do livro "20/20 Foresight: Crafting Strategy in an Uncertain World". Nela, o Courtney afirma:

.

"The financial crisis has actually brought greater clarity because it has forced us to recognize that we have a lot more level three and level four situations than we would have admitted a few months ago. They probably were there all along, yet the bias was toward thinking that issues were more at level one and level two.

...

Maybe the world and the uncertainties we face haven’t changed all that much as a result of the financial crisis, but our perception of risks has. That means there is a real opportunity to rethink the way we make strategic decisions, the way we plan under uncertainty."

.

Este insight é incisivo:"Maybe the world and the uncertainties we face haven’t changed all that much as a result of the financial crisis, but our perception of risks has."

.

"Esta crise talvez não tenha criado nada de realmente novo no mundo dos negócios!

...

Talvez esta crise em que estamos mergulhados a nível mundial não tenha feito mais do que acelerar algo que já estava em curso."

.

Entretanto, o The McKinsey Quarterly publica uma entrevista (A fresh look at strategy under uncertainty: An interview) com Hugh Courtney, autor do livro "20/20 Foresight: Crafting Strategy in an Uncertain World". Nela, o Courtney afirma:

.

"The financial crisis has actually brought greater clarity because it has forced us to recognize that we have a lot more level three and level four situations than we would have admitted a few months ago. They probably were there all along, yet the bias was toward thinking that issues were more at level one and level two.

...

Maybe the world and the uncertainties we face haven’t changed all that much as a result of the financial crisis, but our perception of risks has. That means there is a real opportunity to rethink the way we make strategic decisions, the way we plan under uncertainty."

.

Este insight é incisivo:"Maybe the world and the uncertainties we face haven’t changed all that much as a result of the financial crisis, but our perception of risks has."

sábado, março 07, 2009

No meio não está a virtude, ou seja, não vale guterrear

Há dias escrevi neste espaço:

.

A crise em curso, em boa verdade, não veio trazer novos factores ao cenário.

A crise em curso apenas veio exacerbar as forças, as correntes que já estavam em curso e alterar as fronteiras do meio-termo.

A crise em curso veio alargar as fronteiras do que é o meio-termo pantanoso e traiçoeiro.

A crise em curso veio reforçar a polarização do mercado que já estava em curso, basta recordar The vanishing middle-market.

.

Tendo em conta o que se passa para os consumidores na óptica de Silverstein:

.

"Ao mesmo tempo que essa classe média (fatia mais importante para a maioria das empresas) aspira ao "trading up", cria estratégias de "trading down". Isto é, esses consumidores já não querem o produto de qualidade média, a preço razoável. Preferem comprar um relógio de luxo e equilibrar o orçamento abastecendo a despensa de marcas brancas. É esta a "caça ao tesouro" a que se dedicam e fica o aviso às empresas: já não é no meio que está a virtude, pelo que as que aí estão posicionadas têm de "subir" ou "descer" para não morrerem. "O que fica no segmento intermédio está a ficar sem interesse", sentencia."

.

Não será de esperar o mesmo no B2B? Olhando para as correntes em jogo...

... e reflectindo sobre afirmações deste tipo:

.

"Acha que os problemas de liquidez se vão manter por muito mais tempo?

Acho que sim. Porque, como disse, num plano temos a crise financeira, e logo por baixo dessa temos uma crise ainda mais importante, que é a alavancagem em que o sistema mundial funcionou. O que é que quero dizer? Temos vivido a crédito nos últimos anos, nos EUA, na Europa. Na China e no Japão, a poupança é enorme. Na China, a poupança é de quase 40 por cento, na Europa é de menos de 10 por cento, nos EUA chegou a dois por cento e estava em risco de se tornar negativa. As pessoas estão a viver a crédito nos últimos dez anos. Não é só um problema de confiança, mas de ajustar os níveis de despesa aos níveis de produção."

.

Se o crédito acaba, se o day of reckoning chega para que sejam pagas as dívidas. Terá de haver menos consumo, então, a sobre-capacidade que já existia vai tornar-se em sobre-sobre-capacidade.

.

Como ultrapassar a situação?

.

Muitas empresas não o vão conseguir ponto!

.

As eleitas serão aquelas que vão olhar para o mercado, e isolar grupos específicos, os clientes-alvo, e vão transformar-se para ir ao seu encontro. Não no meio termo, mas fazendo opções: ou preço, ou diferenciação.

.

Cada vez mais ressoam na minha cabeça as quatro questões que Mauborgne e Chan Kim colocam no livro ""Blue Ocean Strategy":

.

"Which of the factors that the industry takes for granted should be eliminated?

.

Which factores should be reduced well bellow the industry's standard?

.

Which factores should be raised well above the industry's standard?

.

Which factores should be created that the industry has never offered?

.

De certeza que a esta migração de valor em curso vai, está a criar, está a destruir, está a reconfigurar os diferentes grupos de clientes-alvo... que novas oportunidades estarão à espera de ser descobertas?

.

Trecho retirado da entrevista de João Salgueiro ao Público de hoje.

.

A crise em curso, em boa verdade, não veio trazer novos factores ao cenário.

A crise em curso apenas veio exacerbar as forças, as correntes que já estavam em curso e alterar as fronteiras do meio-termo.

A crise em curso veio alargar as fronteiras do que é o meio-termo pantanoso e traiçoeiro.

A crise em curso veio reforçar a polarização do mercado que já estava em curso, basta recordar The vanishing middle-market.

.

Tendo em conta o que se passa para os consumidores na óptica de Silverstein:

.

"Ao mesmo tempo que essa classe média (fatia mais importante para a maioria das empresas) aspira ao "trading up", cria estratégias de "trading down". Isto é, esses consumidores já não querem o produto de qualidade média, a preço razoável. Preferem comprar um relógio de luxo e equilibrar o orçamento abastecendo a despensa de marcas brancas. É esta a "caça ao tesouro" a que se dedicam e fica o aviso às empresas: já não é no meio que está a virtude, pelo que as que aí estão posicionadas têm de "subir" ou "descer" para não morrerem. "O que fica no segmento intermédio está a ficar sem interesse", sentencia."

.

Não será de esperar o mesmo no B2B? Olhando para as correntes em jogo...

... e reflectindo sobre afirmações deste tipo:

.

"Acha que os problemas de liquidez se vão manter por muito mais tempo?

Acho que sim. Porque, como disse, num plano temos a crise financeira, e logo por baixo dessa temos uma crise ainda mais importante, que é a alavancagem em que o sistema mundial funcionou. O que é que quero dizer? Temos vivido a crédito nos últimos anos, nos EUA, na Europa. Na China e no Japão, a poupança é enorme. Na China, a poupança é de quase 40 por cento, na Europa é de menos de 10 por cento, nos EUA chegou a dois por cento e estava em risco de se tornar negativa. As pessoas estão a viver a crédito nos últimos dez anos. Não é só um problema de confiança, mas de ajustar os níveis de despesa aos níveis de produção."

.

Se o crédito acaba, se o day of reckoning chega para que sejam pagas as dívidas. Terá de haver menos consumo, então, a sobre-capacidade que já existia vai tornar-se em sobre-sobre-capacidade.

.

Como ultrapassar a situação?

.

Muitas empresas não o vão conseguir ponto!

.

As eleitas serão aquelas que vão olhar para o mercado, e isolar grupos específicos, os clientes-alvo, e vão transformar-se para ir ao seu encontro. Não no meio termo, mas fazendo opções: ou preço, ou diferenciação.

.

Cada vez mais ressoam na minha cabeça as quatro questões que Mauborgne e Chan Kim colocam no livro ""Blue Ocean Strategy":

.

"Which of the factors that the industry takes for granted should be eliminated?

.

Which factores should be reduced well bellow the industry's standard?

.

Which factores should be raised well above the industry's standard?

.

Which factores should be created that the industry has never offered?

.

De certeza que a esta migração de valor em curso vai, está a criar, está a destruir, está a reconfigurar os diferentes grupos de clientes-alvo... que novas oportunidades estarão à espera de ser descobertas?

.

Trecho retirado da entrevista de João Salgueiro ao Público de hoje.

sexta-feira, janeiro 24, 2014

O caso Valbona (parte II)

Parte I..

.

A descrição da Valbona remete-me logo para dois nomes Terry Hill e Wickam Skinner.

.

As empresas existem para servir clientes. Na parte I, na descrição da situação da Valbona, percebe-se o dilema. Se desenharmos o ecossistema da procura

vamos chocar com o poder do dono da prateleira. Os produtos só chegam aos consumidores, aos utilizadores, através da prateleira.

.

A única forma da Valbona chegar directamente aos consumidores é através do marketing. Só através de um marketing forte, associado a produtos genuinamente diferenciadores, é que os consumidores poderão "vergar" o poder do dono da prateleira. O dono da prateleira montou um negócio em torno da eficiência e quer o preço mais baixo. Contudo, sabe que o que realmente interessa é o retorno por m2 de prateleira e, esse retorno, tanto pode ser obtido pela rotação de muitas unidades a um preço baixo, como pela rotação de menos unidades a um preço mais alto (recordar os frangos Purdue e o Evangelho do Valor).

.

O que acontece é que muitas "Valbonas" subestimam-se e desinvestem no marketing, para compensar os "impostos revolucionários" cobrados pela distribuição grande e, por isso, entram numa espiral de perda de valor intangível junto dos consumidores... mas já estou a derivar e a fugir do objectivo deste postal.

.

Voltemos ao ecossistema da procura simplificado lá de cima. Se agora identificarmos o que é que cada interveniente procura e valoriza:

Para ser bom a servir uns, tenho de ser menos bom a servir os outros. Aquilo em que tenho de especializar para servir os "pretos" vai minar a minha capacidade de servir bem os "azuis" e, vice-versa.

Para ser bom a servir uns, tenho de ser menos bom a servir os outros. Aquilo em que tenho de especializar para servir os "pretos" vai minar a minha capacidade de servir bem os "azuis" e, vice-versa.

.

Claro que as "Valbonas" que não pensam chegam à situação espelhada pelas bolas vermelhas:

Não têm uma estrutura produtiva alinhada. Por exemplo, a máquina flexível que permite fazer trocas rápidas de série de produção. não consegue ter a cadência rápida de uma máquina dedicada a grandes séries. Como dar a volta a isto?

Não têm uma estrutura produtiva alinhada. Por exemplo, a máquina flexível que permite fazer trocas rápidas de série de produção. não consegue ter a cadência rápida de uma máquina dedicada a grandes séries. Como dar a volta a isto?

.

Skinner é um velho conhecido, basta pesquisar nos marcadores a sua intervenção neste blogue, por exemplo aqui onde recordo o famoso pwp (plant within the plant):

.

Querer servir o middle-market geralmente resulta em "stuck-in the midlle"

.

Continua com o problema sob o ponto de vista do balanced scorecard.

.

A descrição da Valbona remete-me logo para dois nomes Terry Hill e Wickam Skinner.

.

As empresas existem para servir clientes. Na parte I, na descrição da situação da Valbona, percebe-se o dilema. Se desenharmos o ecossistema da procura

vamos chocar com o poder do dono da prateleira. Os produtos só chegam aos consumidores, aos utilizadores, através da prateleira.

.

A única forma da Valbona chegar directamente aos consumidores é através do marketing. Só através de um marketing forte, associado a produtos genuinamente diferenciadores, é que os consumidores poderão "vergar" o poder do dono da prateleira. O dono da prateleira montou um negócio em torno da eficiência e quer o preço mais baixo. Contudo, sabe que o que realmente interessa é o retorno por m2 de prateleira e, esse retorno, tanto pode ser obtido pela rotação de muitas unidades a um preço baixo, como pela rotação de menos unidades a um preço mais alto (recordar os frangos Purdue e o Evangelho do Valor).

.

O que acontece é que muitas "Valbonas" subestimam-se e desinvestem no marketing, para compensar os "impostos revolucionários" cobrados pela distribuição grande e, por isso, entram numa espiral de perda de valor intangível junto dos consumidores... mas já estou a derivar e a fugir do objectivo deste postal.

.

Voltemos ao ecossistema da procura simplificado lá de cima. Se agora identificarmos o que é que cada interveniente procura e valoriza:

Simplificando podemos dizer que a distribuição grande quer:

- Qualidade no sentido de conformidade, de ausência de defeitos;

- Preço mais baixo;

- Prazo de entrega cumprido.

Que os consumidores se dividem em dois grandes grupos. Os que querem acima de tudo:

- Preço mais baixo;

- Conformidade; e

- Disponibilidade.

E os que querem acima de tudo:

- Inovação, mais qualidade no sentido de mais atributos;

- Novidade;

- Marca que dê confiança, que suporte os tópicos anteriores.

As "Valbonas" que pensam, ao tentar servir a distribuição grande e os dois tipos de consumidores, ao analisarem a sua estrutura produtiva deparam-se com o quadro que aprendi a construir com Terry Hill:

.

Claro que as "Valbonas" que não pensam chegam à situação espelhada pelas bolas vermelhas:

.

Skinner é um velho conhecido, basta pesquisar nos marcadores a sua intervenção neste blogue, por exemplo aqui onde recordo o famoso pwp (plant within the plant):

"For example, if the company is currently involved in five different products, technologies, markets, or volumes, does it need five plants, five sets of equipment, five processes, five technologies, and five organizational structures? The answer is probably yes. But the practical solution need not involve selling the big multipurpose facility and decentralizing into five small facilities.O risco das "Valbonas" que não pensam é o de quererem ir a todos os segmentos e canais, é o de quererem ser uma espécie de "Arca de Noé" e servir o mercado do meio-termo. Contudo esse mercado está a desaparecer por todo o lado... o mundo requer cada vez mais estratégias puras do que estratégias híbridas porque o dinheiro é cada vez mais caro.

.

In fact, the few companies that have adopted the focused plant concept have approached the solution quite differently. There is no need to build five plants, which would involve unnecessary investment and overhead expenses.

.

The more practical approach is the “plant within a plant” (PWP) notion in which the existing facility is divided both organizationally and physically into, in this case, five PWPs. Each PWP has its own facilities in which it can concentrate on its particular manufacturing task, using its own work-force management approaches, production control, organization structure, and so forth. Quality and volume levels are not mixed; worker training and incentives have a clear focus; and engineering of processes, equipment, and materials handling are specialized as needed.

.

Each PWP gains experience readily by focusing and concentrating every element of its work on those limited essential objectives which constitute its manufacturing task. Since a manufacturing task is an offspring of a corporate strategy and marketing program, it is susceptible to either gradual or sweeping change. The PWP approach makes it easier to perform realignment of essential operations and system elements over time as the task changes."

.

Querer servir o middle-market geralmente resulta em "stuck-in the midlle"

.

Continua com o problema sob o ponto de vista do balanced scorecard.

segunda-feira, março 30, 2020

Em que lado do teste do lápis está a sua empresa?

Há anos que recomendo às PMEs a ARTE!

Por exemplo:

Por exemplo:

- Arte, sempre a arte (Maio de 2018)

- O futuro da economia é a arte (Abril de 2018)

- A ascensão do artesão e da arte na produção (parte II) (Abril de 2017)

- Qual a alternativa? (Maio de 2016)

- O papel da arte! (Abril de 2016)

- Arte e PME (Novembro de 2015)

- Acerca da paixão nas PME (Março de 2015)

- Passion Rules!!! (Maio de 2011)

- Há sempre uma alternativa (parte II) (Maio de 2011)

- Paixão e relações amorosas (Fevereiro de 2011)

Há muitos anos que uso a frase:

Há anos que descobri o caso da Viarco:

- Inovação na ponta do lápis (Agosto de 2009)

- Mandamentos para os gestores das unidades com futuro (Novembro de 2009)

- "Nós fazemos as contas ao contrário" (Setembro de 2014)

Estou já na fase final da leitura de um livro simplesmente delicioso, "The Passion Economy: The New Rules for Thriving in the Twenty-First Century" de Adam Davidson. O capítulo 9, “Don’t be a commodity” é acerca de uma empresa que produzia o produto mais commodity que se possa imaginar, lápis escolares, e que depois de ser esmagada pelos chineses deu a volta por cima.

"I came to think of them as exemplifying the single most important rule for thriving in a twenty-first-century economy. The rule applies to manufacturers, but also to bankers and artists and teachers and middle managers at large corporations. The rule is simple: Do not be a commodity.BTW, neste artigo de Julho de 2011, "Uma Sildávia na América", comentei o estado da empresa antes do tal telefonema de Katie

.

Commodities fit a few key criteria. They are undifferentiated. That means that people who buy them don’t see any qualitative difference between competing versions. Instead, commodities are bought based on price and convenience. Most people gravitate toward buying the cheaper dish soap, the cheaper lumber, or the cheaper light bulb instead of the more expensive version on the same shelf.

...

General Pencil had so many orders from so many school districts that it no longer needed to be at the cutting edge of innovation.

The American pencil business had by then become what economists call a mature business.

...

This sleepy world was overturned in the 1990s when something entirely new began to happen. Ships arrived in the nearby Port Newark with huge containers filled with pencils made in China. These pencils looked identical to the ones General made.

...

[Moi ici: Anos depois, a filha do dono da empresa de lápis teve uma ideia] In that moment, Katie realized that she had come upon an enormous hole in the U.S. pencil market. She couldn’t possibly be the only person who wanted a solid, reliable drawing utensil, something between the two extreme options. [Moi ici: Os dois extremos eram os láis chineses de um lado e os de engenharia, de origem alemã] Parents, she knew, would happily pay a reasonable premium for pencils custom-made for their kids. She picked up the phone, called her dad, and offered him an idea that might just save the family business.

Katie eventually created a line of kits that included drawing supplies and instruction books based on her classes.

...

There would be kits with entire lines of colored pencils, and there would be kits with charcoals for high schoolers who had more ambitious goals and wished to develop more comprehensive skills.

...

The companies that shipped container loads of Chinese pencils were too large and distant to worry about such a niche market. They were still satisfied selling commodities. The German companies, which needed to maintain their professional reputation, were reluctant to dilute their brand image by focusing on children. [Moi ici: Como não recordar o truque de Roger Martin para avaliar se uma estratégia é mesmo uma estratégia. O contrário de uma estratégia a sério não é estúpido, mas representa uma brutal fricção para quem a queira seguir] This is why Katie was able to charge a dollar apiece for her pencils. The parents who buy General Pencil kits for their kids are happy to pay a premium, since they are getting a product precisely designed for them.

...

I have come to think of “the pencil test” whenever I am confronted with a question of how best to thrive in a rapidly changing global economy. There is no product more commoditized, more easily reproducible, than the simple No. 2 pencil. Yet General Pencil was able to get out of commodity competition. It was able to thrive and profit by identifying a specific audience with clear needs and serving that audience thoroughly. [Moi ici: Qualquer empresa em Portugal está de um lado ou do outro do teste do lápis. Ou são uma commodity ou são algo com valor acrescentado para um grupo de clientes-alvo que outras empresas nunca poderão oferecer porque estragaria o seu modelo de negócio]

...

[Moi ici: Depois, vem o final do capítulo para fechar este postal, tal como ele começou, a arte] Katie was far more of an artist than an industrialist. Her passion lay in sketching nature, not in looking at spreadsheets, worrying about the rising cost of graphite and the bottleneck at their Midwest distributor. That was stuff her dad loved and would never be for her.

But while working with her dad developing the pencil kits, she found herself becoming fascinated by some of the very things she assumed she’d hate. Distribution, she realized, isn’t just a dull corporate word; it’s the way she can get pencils in the hands of children and artists. Finance isn’t a deathly dull spreadsheet; it’s a language that allows her to make better decisions about the experiments she wants to conduct, and it guides her as she invents different kinds of kits and assesses which ones have successfully found a market. She would never make distribution and finance the core of her work. General Pencil has plenty of experts in those areas. But she learned that there could be as much joy and creativity in business as there is in art."

Subscrever:

Mensagens (Atom)