"Jobs are increasingly viewed as undifferentiated and interchangeable across humans and machines — the very definition of a commodity.

...

Outsourcing — exchanging internal employees for external ones, often offshore — was a big step toward commoditization for many companies.[Moi ici: Mentalidade anglo-saxónica no seu pior, o foco nos custos acima de tudo e, passar ao lado das oportunidades dos nichos e da proximidade]

...

Just as there are low-value and high-value commodities, there are low-value and high-value commoditized jobs.

...

For many jobs, the value is driven less by their intrinsic worth but rather by market demand. A recent Bloomberg Businessweek visual analytic suggests that jobs that disappeared in the first four months of 2017 compared with the same period in 2016 were not lost to automation, but were lost because fewer customers wanted to buy the products and services they produce.

...

For many organizations today, the next big driver of job commoditization is automation driven by smart machines. Simply put, if a job is viewed as a commodity, it won’t be long before it is automated. My research on automation through artificial intelligence (AI) or cognitive technologies suggests that if a job can be outsourced, many of the tasks typically performed by the jobholder can probably be automated — even by relatively “dumb” technologies like robotic process automation. Many global outsourcers are working desperately to create their own automation capabilities that could replace human jobs with machines.

...

The key for financial professionals and other workers whose jobs have traditionally seemed safe is to make themselves less commodity-like. Automation is a game of large numbers, and it’s not economical to automate unique activities. [Moi ici: Mongo é um mundo de "large numbers"?] As long as human workers’ capabilities are differentiated from machines’ capabilities, then machines can’t easily replace them — and few organizations will be tempted to automate that niche."

quarta-feira, agosto 09, 2017

"Automation is a game of large numbers"

"uma tendência a considerar para a cidade do futuro"

Há dias em "One more time, it is not about cost" escrevi:

"Antes de me sentar a citar este texto dei uma caminhada de 5km por ruas secundárias de Mafamude que não visitava desde 1973. A certa altura olho para uma série de "lojas": uma de imobiliário, uma híbrida entre a mercearia e a chinesa, uma como ginásio de educação, outra de ... e veio-me à mente o pensamento de que reconheceremos Mongo quando começarem a aparecer nos espaços de loja: unidades de fabricação com 2 ou 3 trabalhadores e tecnologia."Agora encontro:

"The Garment District is no different; it is an industrial zone, with other nonindustrial uses allowed. But since fashion is a lighter industry, like other niche design-driven industries, it is actually clean and quiet and can be easily integrated with office and residential uses in the same buildings. [Moi ici: E o que é Mongo senão um paradigma de empresas dedicadas a servir nichos?] What if the higher-value residential tenants could consciously support the lower-rent garment tenants (or other light manufacturing spaces) through cross-subsidies? The result would be a diverse mix of making, selling, playing, and living; creating a 24/7 work-live community. The ground floor could remain retail space relating to the supplies that comprise the products—buttons, zippers, sequins, fabrics—while the lower and middle floors, where the showrooms are often located, would be required to be maintained as factories. The upper floors could contain the higher-value showrooms, and commercial and residential units.Afinal não é uma loucura de anónimo da província, se calhar é uma tendência a considerar para a cidade do futuro.

...

Another approach is to make the garment workers visible, injecting energy into the area with new physical transparency, exposing the industrial mysteries of workers making patterns, cutting, sewing, and pleating fabrics, in what I call the “consumption of production.” The emergence of industry-as-spectacle combines retail with making, so that the consumer also can see into the process from beginning to end, in our experience economy. This would be part of a longtime tradition of urban merchants and their workshops, or even the phenomenon of open kitchens in restaurants, and follows new interests in authenticity. In this new context, it combines another hybrid of retail-factory spaces for urban chocolatiers, coffee roasters, and bakers bringing street life to cities. In doing so, we can redefine and bolster the dynamism and diversity of our innovative and productive city."

terça-feira, agosto 08, 2017

Acerca do reshoring

"One is the notion of reshoring: some Western manufacturers are “bringing manufacturing back home,” but our understanding of why exactly this occurs is limited.

...

Location decisions must be understood not just through the lens of economic attractiveness of one region or country over another, but also as a decision where many organizational and technological interdependencies become relevant: decisions about where to locate manufacturing link to other decisions, such as location of research and development activities with other value chain activities and actors, such as product development, suppliers, and markets.

...

When and why should policy makers be interested in production location decisions? Understanding value creation is central to understanding the role of production both within a firm and within a national economy.

...

Our results suggest that contemporary location decisions link intimately to three dimensions of interdependence with suppliers, market, and development activities: formalization, coupling, and specificity.

...

...Mongo implica mais proximidade e interacção com clientes e fornecedores, e maior rapidez na evolução da produção e do desenvolvimento.

we find the proposition that coupling is the most important source of interdependence in location decisions plausible. Specifically, if production is tightly coupled with development, relocating one implies relocating the other. In contrast, low formalization of the Production- Development Dyad may make it easier to manage the relationship if the two activities are geographically collocated, but coordination can succeed even without collocation as well.

We also observe that the common denominator in the cases where production takes place only in the low-cost country is high formalization combined with low specificity. This is not surprising: It is specifically the routinized, generic forms of production that become candidates for both outsourcing and offshoring.

...

In our analysis of the 35 location decisions, the key theme that repeated itself throughout the cases was the notion of interdependence of activities. As a general finding, this is hardly surprising, but the detailed understanding of how formalization, specificity, and coupling link to location decisions has the potential to both inform firm-level strategies and to at least introduce new vocabulary into discussions of economic policy."

Trechos e imagem retirada de "Why locate manufacturing in a high-cost country? A case study of 35 production location decisions" publicado por Journal of Operations Management 49-51 (2017) 20-30

Marcas: Hara-Kiri

"Overproduction is a huge problem that the industry tries to hide as it chases after fake numbers and reports of constant growth.

...

The industry talks about conspicuous consumption — buying for the sake of buying — as the reason behind the growth in the luxury segment. But brands are producing more product than there is demand for. I call it conspicuous production, producing for the sake of producing and artificially inflating the numbers.

...

Supply meets demand is the basic rule of business and one the whole industry seems to ignore. Sales are the first indicators of overproduction. The goal should be to reach 100 per cent sell-through before discounts, though figures over 90 per cent are acceptable, as no one can predict the exact demand down to each SKU [stock-keeping unit]. What’s shocking is that most brands in big stores don’t even sell 20 per cent of their merchandise before discount, yet continue to report wholesale growth.

.

Stores and brands are trying to hide the truth by opening outlet stores, which sell unsold merchandise and sometimes even similar collections that never went to the full-price retailers. Outlet stores then have the same problem: they end up with deadstock that they resell to other countries and the same scenario repeats itself. If nobody wanted something full-price, it doesn’t necessarily mean that anyone will want it half-price. Recent reports show that more than 30 per cent of merchandise produced by fashion brands will never be sold. The clothes end up in landfill. It affects consumer buying behaviour as well. Pieces bought on discount appear to be less valuable psychologically to the consumer, which makes it easier to throw them out.

...

Luxury is like dating. If something is available and in front of you, it’s less desirable. Scarcity is what defines it. One of the ways to create scarcity is to reduce the supply curve. The more demand there is, the more desire it creates. Desire is the key value in luxury business.

...

The parallel market is one of the dirtiest secrets of the fashion industry. [Moi ici: Outro tema de que me falaram na conversa na origem de "Em busca de um novo oásis"] More and more luxury stores have become a beautiful façade to cover the real business going on behind the scenes. In addition to selling a small part of the merchandise directly to the final consumer, they also play an intermediary role in reselling the biggest part of their order to horrible stores, often in remote locations all around the world, which cannot get brands through the official channels.

...

Brands are perfectly aware of the parallel market, and the stores involved in it, but are closing their eyes in order to further report growing sales numbers. Officially those brands are sold only in the best stores in the world, and claim a limited and exclusive distribution, but in reality their merchandise ends up in horrible places. There is a certain obsession with reporting the growth for fashion brands no matter what the true cost.

...

The values and goals have mutated so much that things that simply make sense start to look abnormal or disruptive. Historically, brands produced clothes to sell to a final consumer. Today brands produce runway collections to sell a perfume or a wallet in a duty-free store. They stuff stores with unwanted merchandise to report artificial growth. They keep overproducing while talking about sustainability. They claim exclusive distribution while paralleling their own merchandise. They are slowly killing their brands in the long term to have a quick profit today."

Interessante, relacionar a legenda das figuras do artigo de donde retirei estes trechos "Vetements: the gospel of Guram Gvasalia":

"they chose to shoot their designs on local people and families living in the area"Com este outro artigo "QUORA: IS VICTORIA'S SECRET FAILING? IT'S NOT LOOKING GOOD":

"The first clear indication that it’s the perfection in Victoria’s Secret images that is proving to be a turnoff was the emergence of competitor Aerie, whose marketing plays up its “unretouched, real women” angle. Ever since it launched its no-airbrushing policy in 2014, Aerie’s sales have taken off.Autenticidade versus "fake"

...

As a policy, Curvy Kate does not use any professional models, sourcing the eclectic mix of women it features from social media.

.

Also going the real-women, no-Photoshopping route and winning reams of positive reviews is LONELY LINGERIE, which a few months ago placed a 56-year-old woman at the centre of their campaign."

segunda-feira, agosto 07, 2017

Deixam-me a pensar

Um anónimo da província entretem-se a diletar:

Trechos retirados de "Impetus. O ‘underwear’ de Casillas está a investir 3 milhões"

"O conhecimento técnico, a aposta, constante, na qualidade, nos detalhes e no estabelecimento de “relações de confiança e de transparência” têm sido os grandes pilares de desenvolvimento da Impetus no mundo. A par da inovação. O grupo conta já com vários produtos patenteados e linhas específicas para desporto, com tecnologia que regula a humidade e transpiração, além das gamas Innovation (linha que armazena o calor corporal excessivo e volta a distribuí-lo em caso de necessidade, uma tecnologia desenvolvida pela NASA para os astronautas), Thermo (para proteger do frio, no inverno) e ProtectDry (roupa interior para incontinentes, lavável e reutilizável, e com tecnologia que elimina odores). Este último é um produto que está a ser vendido, em força, na grande distribuição, com destaque para Portugal, Espanha, Suíça, Alemanha, EUA e Suécia e com entrada, em breve, na Rússia e na África do Sul.Recordar:

...

O Citeve e a Universidade do Minho são parceiros de excelência em I&D. Recentemente, chegou ao mercado a linha de roupa interior com certificado orgânico, que garante um fabrico socialmente sustentável e sem uso de químicos.

...

O objetivo é o aumento da capacidade produtiva por via da aquisição de novos equipamentos, alguns dos quais completamente inovadores no país

...

A consolidação de mercados é a grande prioridade da Impetus, que exporta 98% do que produz, com especial destaque para mercados como Espanha, França, México, Japão, Estados Unidos, Alemanha, Suíça e Noruega, estes últimos em regime de subcontratação para outras marcas, o chamado private label, caso da Calvin Klein ou da Tommy Hilfiger, entre muitos outros. A marca própria vale 25%.

...

Mas o private label, mesmo incerto, é o que nos tem mantido até aos dias de hoje."

- Especulação (parte III) (Agosto de 2008)

- É a crise, outra história portuguesa... (Outubro de 2011)

- Spin-off à vista? (Dezembro de 2011)

No que fico a pensar?

Algo que passou na conversa que deu origem a este postal da semana passada "Em busca de um novo oásis": a fraqueza relativa das marcas próprias (comparar com a opinião de 2011) e o crescente encanto com o private label, talvez por causa do ruir do retalho tradicional.

E volto aquela preocupação de Dezembro de 2011. Assim como na série "Uma coisa é uma coisa e outra coisa é outra coisa" abordo a relação entre estratégia e estrutura produtiva, este artigo onde se fala de investigação e de "grande distribuição" e o de Dezembro de 2011, deixam-me a pensar se não há algo a melhorar a nível de relação entre estratégia, propostas de valor e estrutura de vendas.

Trechos retirados de "Impetus. O ‘underwear’ de Casillas está a investir 3 milhões"

Beyond Lean (parte II)

Na parte I procurámos demonstrar que o futuro será muito mais do que a automatização. A explosão de tribos de Mongo requer estruturas produtivas com um ADN diferente do que aquele que o século XX nos legou.

A evolução tecnológica vai trazer, também, a democratização da produção, a redução de barreiras à entrada e, por isso, a explosão no número de pequenas empresas life-style business.

Em paralelo a esta evolução, que vai sugar os mais apaixonados para uma nova Idade de Ouro de artesãos do século XXI, teremos a reacção das empresas grandes no seu combate final pelo domínio da decrescente fatia de mercado que representa os que continuam dentro da caixa e optam pelo preço como o critério prioritário de compra. Essas continuarão a optar pela automatização como forma de reduzir custos.

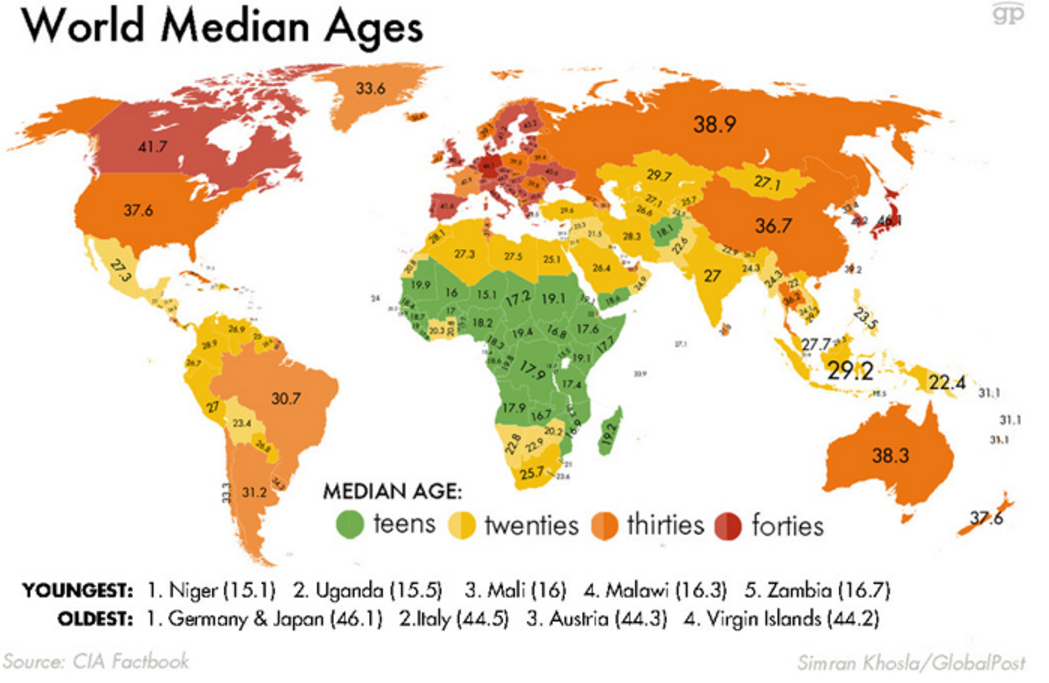

E em paralelo com as duas correntes anteriores teremos uma terceira impulsionada pela demografia e tão bem ilustrada em "Rise of the machines".

Até que ponto Portugal vai ter de ser pioneiro nesta terceira via?

Demografia, marxismo social e a atracção pela emigração, são uma combinação tremenda que só agora começa a ter o seu impacte. Recordar:

domingo, agosto 06, 2017

Pedir uma explicação para esta "blasfémia"

Numa introdução mais humorada posso dizer que descobri a identidade secreta do @nticomuna. Só duas pessoas poderiam escrever algo que se escreve neste artigo do Financial Times, "Sterling’s Brexit slide has yet to deliver trade’s sunlit uplands", ou o @nticomuna ou eu. Como não fui eu, ergo ...

"Brexit, we were told, will improve Britain’s trade performance through the depreciation of sterling.Interessante mesmo era alguém pegar neste artigo do FT e com ar de ingénuo chegar junto do bicicletas, ou de Ferreira do Amaral, ou de Vítor Bento, e pedir uma explicação para esta "blasfémia" de exportações que crescem com moeda a fortalecer.

...

The big difference is currency movements. Sterling has fallen 17 per cent since late 2015 against Britain’s trading partners, a period in which the equivalent measure for Portugal rose 2 per cent. With such stark exchange rate differences, it would be natural to see net trade — exports minus imports — contributing more to Britain’s growth rate than that in Portugal over the past year. UK imports have become pricier and exports more competitive.

.

But in most recent data comprising the year to the first quarter of 2017, net trade subtracted 0.2 percentage points from the UK’s growth rate while adding 0.5 percentage points to Portugal’s rate. Sterling’s slide has not helped Britain.

.

Between January and March this year UK output in production industries expanded 2.3 per cent compared with a year earlier, the same rate as the growth in services and less than in construction. British rebalancing towards production is notable for its absence. In Portugal, industrial output grew 4.8 per cent over the same period, considerably faster than the 2.8 per cent overall growth rate. Brexit has not given the UK a more balanced economy.

.

Surely, at least, the Leave vote has spurred UK companies to broaden their horizons and focus exports outside the EU? Again, no. With the depreciation allowing exporters to raise prices, British export values to the EU27 were 15.5 per cent higher in the year to the first quarter, a more rapid improvement than the 13.8 per cent growth rate to non-EU countries. But compared with Portugal, these figures look disappointing; over the same period its exports to outside the EU grew 33.2 per cent with a 51.6 per cent rise in US exports.

.

These are the sort of numbers that would have Brexiters salivating, if they related to Britain rather than Portugal."

Prefere gasolina no Intermarché ou na BP?

Prefere gasolina no Intermarché ou na BP?

A pergunta faz tanto sentido como a pergunta "Prefere um voo barato ou… um voo pontual?"

A resposta é: depende?

Tudo depende do contexto, tudo depende do objectivo que se pretende atingir.

Costumo ir a Guimarães uma vez por semana, trabalhar numa empresa. Prefiro ir de comboio ou de carro?

Pela poupança, pela comodidade, pelos minutos "com mãos" ganhos vou quase sempre de comboio. Também vou de carro quando tenho um horário apertado e conciliar uma ida a Guimarães com uma ida a Felgueiras.

Por isto é que a caracterização dos clientes com base na idade e noutros atributos independentes do contexto não são muito úteis para prever comportamentos.

A pergunta faz tanto sentido como a pergunta "Prefere um voo barato ou… um voo pontual?"

A resposta é: depende?

Tudo depende do contexto, tudo depende do objectivo que se pretende atingir.

Costumo ir a Guimarães uma vez por semana, trabalhar numa empresa. Prefiro ir de comboio ou de carro?

Pela poupança, pela comodidade, pelos minutos "com mãos" ganhos vou quase sempre de comboio. Também vou de carro quando tenho um horário apertado e conciliar uma ida a Guimarães com uma ida a Felgueiras.

Por isto é que a caracterização dos clientes com base na idade e noutros atributos independentes do contexto não são muito úteis para prever comportamentos.

sábado, agosto 05, 2017

Beyond Lean

Há anos que escrevo aqui sobre o advento de Mongo e o consequente impacte na dança entre produção e consumo:

- mais tribos;

- mais nichos;

- séries mais pequenas;

- mais flexibilidade;

- mais rapidez;

- mais variedade;

- mais diferenciação;

Em paralelo há anos que se lê com cada vez mais frequência sobre a automatização da produção.

Em Mongo, a produção é muito diferente da do paradigma do século XX com séries longas e planeamento da produção feito com muita antecedência. Em Mongo o planeamento da produção é feito cada vez mais em cima e é mais volátil. Como é que a automatização e as organizações-cidade lidam com Mongo?

"With improvements in living standards and a transformation in people’s ideas of consumption, much of the current electronics manufacturing industry is confronted with market demands characterized by variety and volume fluctuation. Manufacturing system flexibility is useful to address such fluctuated market demands.Anónimo da província mas muito à frente:

...

Seru production has been called beyond lean in Japan and can be considered to be an ideal manufacturing mode to realize mass customization

...

seru production relies on low-cost automation and has little automation. When reconfiguring a conveyor assembly line into serus, expensive large automated equipment is substituted with simple-structure equipment with similar functions. The reconstructed equipment can be easily duplicated and modified at a low cost, so as to avoid equipment-sharing conflicts among multiple serus and reduce investment in equipment.

...

Factories that produce multiple electronics product types in small-lot batches tend to adopt seru production. Compared to mass production, which displays its superiority in the case of a narrow range of product types with high product volumes, seru production would be affected by low efficiency and high cost in such an environment.

...

Using highly automated production systems, mass production factories can attain high production efficiency. However, they usually achieve low production flexibility. As both the variety and volume fluctuations of market demands increase, mass production factories may need to reconfigure their traditional conveyor assembly lines for their survival and development.

...

Seru production is human-centered manufacturing. Multiskilled operators are important resources to implement seru production, more important than in mass production. The equipment used in seru production is simple and not automated. The effect and influence of equipment on the performance of seru production systems is less than that on mass production systems. Accordingly, a practical production planning system for seru production should consider multiskilled operators more than equipment. In a dynamically changing manufacturing environment, a dynamic production planning system is needed"

- Um mesmo processo automatizado é demasiado rígido para Mongo

- Mongo e a automatização... pois!

- "mas o essencial é que o mercado de massas desapareceu"

Cuidado com os media, desconfie sempre!

Trechos retirados de "An implementation framework for seru production" publicado por Intl. Trans. in Op. Res. 00 (2013) 1–19

Tribos por todo o lado

Tribos por todo lado, nichos por todo o lado. Mongo é isto:

Trechos retirados de "The Cult of the Line: It’s Not About the Merch"

"all of them into this niche product that acts as a social identifier. For them, standing in line for a T-shirt or baseball cap is a way of telling the world that you know about something that not everyone is hip to.

...

“We become a little band of survivors, with a grim gallows humor to match,” Mr. Andrews wrote. “We’re all in this together.”"

Trechos retirados de "The Cult of the Line: It’s Not About the Merch"

sexta-feira, agosto 04, 2017

Outro festival de blasfémias

Continuado daqui.

Agarre-se às cadeiras, segue-se mais um festival de blasfémias:

Agarre-se às cadeiras, segue-se mais um festival de blasfémias:

"The alternate to costly multipurpose or special-order machines is inexpensive, slower, and fewer-purpose machines, but many of them. Every work cell that needs one gets one and can then function autonomously. Although a multipurpose machine offers high flexibility through quick changeover and rapid production rate, all else equal, conventional fewer-purpose machines might provide even greater flexibility when employed in a number of manufacturing cells. Conventional machines are also simpler to operate and less costly to maintain.”[Moi ici: Pode estar aqui uma oportunidade para os fabricantes portugueses de máquinas?]Trechos retirados de "Missing link in competitive manufacturing research and practice: Customer-responsive concurrent production" publicado por Journal of Operations Management 49-51 (2017) 83-87

Constraining that three-pronged potential, however, is the tendency of manufacturers to retain SP practices in spite of their limited responsiveness. Such dysfunctional decision making ... tends to be chosen for local efficiency rather than effectiveness - remains in force today.

Several authors emphasize the importance of avoiding monument equipment consider the potentially negative impact on responsiveness of smoothing the production schedule as commonly

...

concurrent production relies on multiple, relatively slow-paced, simple, small-footprint, low-cost productive units, sometimes referred to as right-sized

...

As the number of production units increases, so does the degree to which production becomes concurrent with demand; and as the degree to which equipment units are dedicated increases, so does concurrency.

...

“Abolish the Setup,” points to the liabilities of “a single, expensive machine that can produce many kinds of parts,” compared with several less-expensive, dedicated machines.

Small, inexpensive units of capacity can be readily reconfigured, which grows in importance as customer preferences proliferate.

...

CP builds factory infrastructures around multiple product-family or customer-family-focused units - cells, machines, production lines, plants-in-a-plant - with simple, compact, low- cost, “right-sized” equipment and avoidance of monument-sized equipment. The primary objectives of CP are to reduce customer lead times and distribution inventories. Longer-range benefits to the organization as a whole include better customer retention, market penetration, and sales growth. In an era when customers increasingly demand higher variety from manufacturers, CP is timely, making it possible to reap the benefits of responsiveness while keeping production costs low enough for competitiveness."

"associar-se a um propósito"

Ontem, quando li o título "As marcas já não querem só vender produto, querem vender um propósito." lembrei-me logo de dois postais:

E lembrando-me do job to be done e "Your customers care about the progress they will make" escrevi no Twitter:

"As marcas já ñ querem vender só um produto. Querem vender um propósito"— Carlos P da Cruz (@ccz1) August 3, 2017

IMHO ñ é bem isto.

Creio q é +: Querem associar-se a 1 propósito

Em vez de querer vender um propósito, associar-se a um propósito que o cliente já persegue e valoriza

quinta-feira, agosto 03, 2017

Em busca de um novo oásis

"Portugal está a perder terreno face a Itália no que à produção e exportação de calçado diz respeito.Quando li este trecho, meio a correr, pensei logo na evolução do perfil da produção portuguesa como forma de justificar esta evolução. Recordar a série "Comparações enganadoras"

...

é no preço médio que a diferença se acentua: 26,09 dólares por par, pouco mais de metade dos 47,76 euros a que são exportados os sapatos italianos."

Depois, quando li com atenção o resto artigo encontrei uma comparação mais útil:

"no calçado de couro, o fosso face a Itália agravou-se: os sapatos italianos de couro são exportados, em média, a 63,78 dólares, mais 2,28 dólares do que em 2015, enquanto os portugueses não vão além dos 31,16 dólares, praticamente o mesmo valor do ano anterior."Como é que o artigo explica esta evolução?

"“uma parte significativa do diferencial de preços” é explicado pelo facto de Itália ter uma posição muito superior à portuguesa nos mercados extracomunitários, que registam, habitualmente, preços médios de exportação superiores aos europeus."Esta explicação parece-me tão simplista...

Em interessante conversa com alguém que pensa o sector encontrei explicações muito mais plausíveis, IMHO.

O calçado português com marca própria, embora tenha um peso muito baixo na quantidade produzida, tem um preço à saída da fábrica bem mais alto. Onde se vendem essas marcas? No retalho tradicional. O que é que está a acontecer ao retalho tradicional? Recordo este trecho que escrevi em Abril passado:

"A evolução do retalho é um tema que me interessa porque é super importante para as PME com que trabalho. A maioria das PME portuguesas não tem marca própria relevante. Ou produzem para marcas de outros ou produzem componentes que serão incorporados nas marcas de outros (B2B2C ou B2B2B2C).A revolução do retalho tradicional disrupciona as cadeias de fabrico.

.

Assim, o seu futuro depende em larga escala, segundo o modelo de negócio actual, do sucesso da última interacção da cadeia, aquele ...B2C. Se esta última interacção falhar, tal como falharam em massa as sapatarias de rua quando chegaram os centros comerciais, as nossas PME terão um problema em mãos."

Primeira explicação: a disfunção do retalho tradicional. Se os clientes dos clientes deixam de comprar, os fornecedores ficam sem procuram.

Segunda explicação: o impacte do reshoring e a tentação pelo caminho mais fácil.

"O regresso da produção industrial à Europa vai voltar a colocar em cima da mesa a hipótese de apostar no low-cost. E o low-cost parece tão intuitivo, tão atraente..."Ainda esta semana um empresário me contava que um seu cliente tinha recebido um encomenda muito grande de meios de produção para o fabrico de calçado. Algo que relacionei com uma visita de há alguns meses de alguém que procurava empregas muito grandes em Portuga para produzir calçado.

Neste momento, a primeira explicação é a que mais me preocupa. Daí a escolha da expressão "placa teutónica" e o recurso à imagem do equilíbrio pontuado. O mundo mudou e agora é preciso correr atrás do prejuízo para voltar a encontrar um novo oásis.

BTW, uma terceira explicação o abandono do couro.

Trechos retirados de "Preço do calçado português é quase metade do italiano"

O anónimo da província estava certo!

Mais um texto em linha com o que aqui defendemos há anos com base na nossa experiência empírica. Enquanto os membros da tríade (académicos fechados nas suas torres de marfim, comentadores económicos e políticos) continuam a falar de competitividade com base no século XX e, por isso, estão prisioneiros do eficientismo e das manigâncias com a cotação da moeda, há um outro mundo:

Continua.

Trechos retirados de "Missing link in competitive manufacturing research and practice: Customer-responsive concurrent production" publicado por Journal of Operations Management 49-51 (2017) 83-87

"The manufacturing arm of operations management (OM) has limited itself to a narrow vision of what this key organizational function is supposed to be and do. OM scholars have quibbled about efficiency in factory and supply-chain operations, while giving little attention to tying production forward to end customers. Our view is that this single-minded focus on efficiency has effectively knocked OM research, theory, topics, methods, measures, and practitioner guidance off kilter.Agora metam neste cenário os fanáticos da automatização que só pensam no eficientismo e se esquecem de Mongo: rapidez, flexibilidade e variedade crescente para servir tribos cada vez mais exigentes.

On the industry side, a narrow view of OM mirrors the single- minded focus that we observe in academia. Manufacturers proudly display factories that have been cleared of targeted wastes and are marvels of short flow times, low work-in-process in- ventories, and high capacity utilization. They may also point to similar achievements with key suppliers. A closer look, however, often reveals a supply chain with extended lead times [Moi ici: Aposto que, como eu, não sabia que o Toyota Production System, essa maravilha de organização e eficiência (sem ironia) congela a previsão de produção com 8 semanas de antecedência] and swollen finished-goods inventories that dwarf the low in-plant inventories. The overall supply chain often loses the ability to compete on anything except cost. The resulting vulnerability to low-cost competition leads to offshoring.

Inability to synchronize with downstream demand increases production cost through supply-demand mismatches, delays in addressing quality issues - even mass product recalls, and customer defections. These negative outcomes are commonplace even in factories held up as bastions of “best practices”.

...

A major deterrent to CP [Moi ici: Concurrent production] adoption is the tendency both in companies and among the OM academic community to focus on localized efficiency to the neglect of responsiveness in fulfilling customer needs. Manufacturing people have limited interaction with final users, so the cost of valuing efficiency above responsiveness goes unnoticed. In consequence, manufacturing-improvement efforts tend to be limited to pursuit of within-factory efficiencies: short internal flows, smoothed sched- ules, and high capacity utilization.

...

manufacturers in their quest for operational efficiency prefer factory operatives to be always busy making products. CP, on the other hand, welcomes the situation in which both equipment and its operators are idle for lack of current demand.

...

Another managerial mindset that hinders CP implementation is the assumption that it is better to reduce changeover times on a single piece of equipment than to duplicate that equipment. Along similar lines, we have seen manufacturers replacing multiple units with a single large, flexible piece of equipment. ... done for the sake of “... improved efficiency and productivity”. This way of thinking culminates in “monument” machines: high-speed, multi-functional equipment that gives the impression of being extremely efficient. ... that engineers “... typically think at the process level,” seeking efficiencies “... by combining operations with[in] a single piece of equipment.” This “can cause a disconnect with general management who want to increase sales, make gains in market share, or find new sources of revenue by adding product lines.”"

Continua.

Trechos retirados de "Missing link in competitive manufacturing research and practice: Customer-responsive concurrent production" publicado por Journal of Operations Management 49-51 (2017) 83-87

quarta-feira, agosto 02, 2017

Um preço é um palpite!

O @icyView no Twitter chamou-me a atenção para este texto "Fairness or efficiency?" que mereceu este comentário da minha parte:

Quando é que as pessoas vão aprender que o preço não resulta de uma equação? Quando é que as pessoas vão perceber que o preço não depende do custo? Quando é que as pessoas vão aprender que o preço não é justo nem injusto? Quando é que as pessoas vão aprender que um preço é um palpite?

E os palpites são verdadeiros ou falsos hoje e, depois, falsos ou verdadeiros amanhã. Por isso, gosto da frase: os preços são contextuais. Porque os preços são contextuais, recomendo às empresas que contribuam para o contexto:

Quando é que as pessoas vão aprender que o preço não resulta de uma equação? Quando é que as pessoas vão perceber que o preço não depende do custo? Quando é que as pessoas vão aprender que o preço não é justo nem injusto? Quando é que as pessoas vão aprender que um preço é um palpite?

E os palpites são verdadeiros ou falsos hoje e, depois, falsos ou verdadeiros amanhã. Por isso, gosto da frase: os preços são contextuais. Porque os preços são contextuais, recomendo às empresas que contribuam para o contexto:

Análise de risco à la FMI

Risco - o que a incerteza pode gerar se não mexermos.

Oportunidade - o que podemos ambicionar se mexermos?

Imagem retirada de "Italy : 2017 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Italy"

terça-feira, agosto 01, 2017

Um festival de blasfémias!!!

Em "Talvez o tema que mais nos separa dos níveis de produtividade do resto da Europa Ocidental" incluí esta figura:

Curioso, fui à procura do último livro do John Mullins referido na entrevista.

Encontrei "The Customer-Funded Business: Start, Finance, or Grow Your Company with Your Customers’ Cash". Um festival de blasfémias, tal o distanciamento face à cultura mainstream acerca das startups e do empreendedorismo, transformada num concurso de beleza para cativar investidores e financiadores em detrimento da cativação de clientes.

Esta manhã, entre as 7h30 e as 8h30 tive a oportunidade de ler o primeiro e o oitavo capítulos:

Curioso, fui à procura do último livro do John Mullins referido na entrevista.

Encontrei "The Customer-Funded Business: Start, Finance, or Grow Your Company with Your Customers’ Cash". Um festival de blasfémias, tal o distanciamento face à cultura mainstream acerca das startups e do empreendedorismo, transformada num concurso de beleza para cativar investidores e financiadores em detrimento da cativação de clientes.

Esta manhã, entre as 7h30 e as 8h30 tive a oportunidade de ler o primeiro e o oitavo capítulos:

"I believe raising equity at the outset of a new venture’s journey is, at least most of the time, an exceedingly bad idea—for both entrepreneurs and investors alike.Não consigo deixar de pensar que o entrevistado, ao recomendar o livro de Mullins o fez com um sorriso maroto.

...

[Moi ici: Segue-se um argumento que há anos uso no Twitter, sobre o tema] waiting to raise capital forces the entrepreneur’s atten- tion toward his or her customers, where it should be in the first place.

...

making do with the probably modest amounts of cash your customers will give you enforces frugality, rather than waste. Having too much money can make you stupid and lets you ignore your customer! Having less money will make you smarter, and will force you to run your business better, too.

...

focusing your efforts to raise cash from customers who are willing and eager to buy from your yet-unproven com- pany is likely to mercifully put to rest a half-baked or not- quite-right idea that requires more development—a pivot, in today’s entrepreneurial lexicon—in order to hit the mark.

...

“We think that you shouldn’t start with the assumption that you need to raise money . . . Huge companies have been created with little or no outside investment.”

...

- Raising capital demands a lot of time and energy, distracting entrepreneurs from building the actual business.

- Raising capital too early means pitching the merit of the business idea to potential investors, rather than proving its merit among customers in the marketplace."

Um exemplo muito mais útil para as PME portuguesas

Um exemplo concreto de como uma empresa com um mínimo de recursos conseguiu uma presença na internet, em "Valentina, moda ‘low cost’ y redes sociales para pasar de 200 euros a diez millones en tres años".

Um exemplo muito mais útil para as PME portuguesas que se queiram aventurar na internet do que os casos de multinacionais americanas ou europeias.

Um exemplo muito mais útil para as PME portuguesas que se queiram aventurar na internet do que os casos de multinacionais americanas ou europeias.

segunda-feira, julho 31, 2017

Pensar com os pés assentes na terra

No caderno de Economia do semanário Expresso deste fim de semana, no meio do artigo "As quatro vidas da Fitor: De estrela da Bolsa a 20 empregados" destaco dois trechos:

O primeiro porque contrasta com a leviandade dos políticos na torrefacção de dinheiro impostado e segue um exemplo tão comum nas PME com que trabalho: prudência. Como não recordar a America Latina Logística e a sua regra nº 4. Gente que não está de turno só até à próxima eleição pensa com os pés assentes na terra.

O primeiro porque contrasta com a leviandade dos políticos na torrefacção de dinheiro impostado e segue um exemplo tão comum nas PME com que trabalho: prudência. Como não recordar a America Latina Logística e a sua regra nº 4. Gente que não está de turno só até à próxima eleição pensa com os pés assentes na terra.

O segundo porque é mais um exemplo da pregação deste anónimo da província:

O segundo porque é mais um exemplo da pregação deste anónimo da província:

"abandonar as referências mais básicas, [Moi ici: As que vendem pelo preço e requerem o custo mais baixo] estar atento às tendências do mercado e apostar numa oferta com mais valor acrescentado, [Moi ici: Subir na escala de valor. What else?]"

Competir pela flexibilidade

No caderno de Economia do semanário Expresso deste fim de semana, no meio do artigo "PAdira ganha músculo financeiro com a Sonae" encontro este trecho:

Parece retirado deste blogue. Há anos e anos a defender que se não podemos competir pelo custo temos de competir pela flexibilidade, pela co-criação, pela interacção.

Está a entranhar-se. Quantos anos demorará a chegar às sebentas?

Primeira medida Sonae para a Adira? Sugiro tirá-la daquele local, colocá-la em zona industrial e vender o terreno para imobiliário, apesar do cemitério.

Parece retirado deste blogue. Há anos e anos a defender que se não podemos competir pelo custo temos de competir pela flexibilidade, pela co-criação, pela interacção.

Está a entranhar-se. Quantos anos demorará a chegar às sebentas?

Primeira medida Sonae para a Adira? Sugiro tirá-la daquele local, colocá-la em zona industrial e vender o terreno para imobiliário, apesar do cemitério.

Subscrever:

Mensagens (Atom)