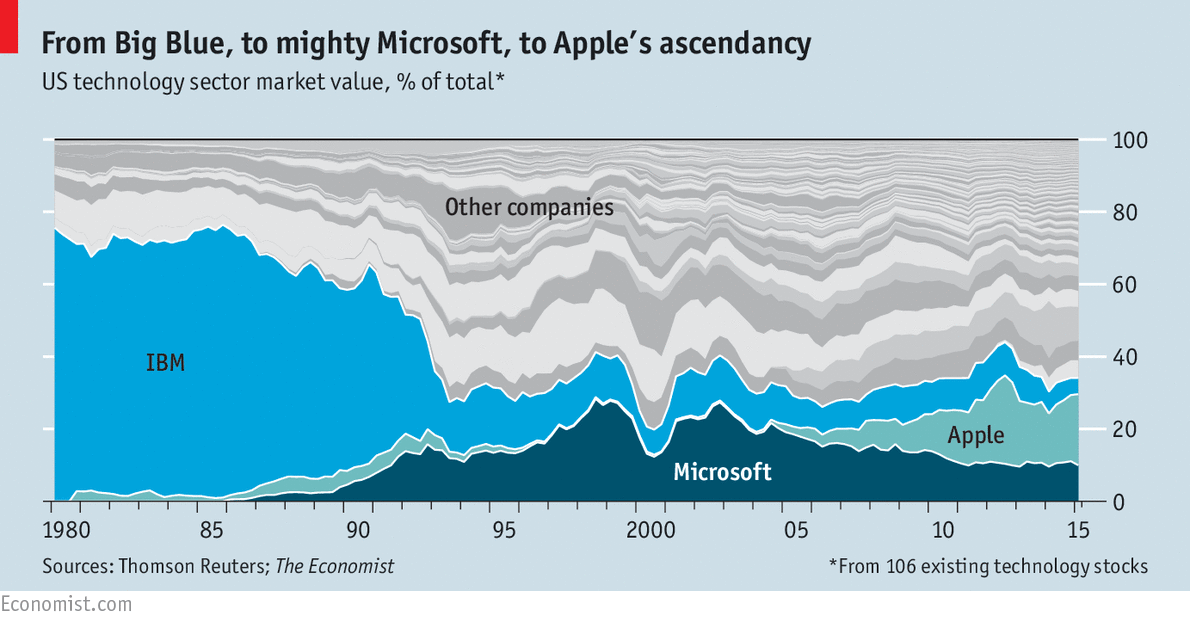

Primeiro, este trecho de Trout em "Differentiate or Die: Survival in Our Era of Killer Competition":

"Now let’s look at that 0 percent differentiation degree in the Banking sector. How can that be? All these big name banks spend millions on advertising telling us how wonderful they are to do business with. Well, class, the answer is obvious. Mergermania has taken a terrible toll. And after all these mergers, who knows who is who these days much less for what they stand. As the psychologists advise, without a line to the past, how can you be sure of a line to the future. The Banking category is a mess and deserves their 0 percent."

O que ouvimos e lê-mos em Portugal sobre os bancos?

.

.

Corrida para fechar agências!

.

Corrida para passar a oferecer os serviços via internet!

.

O que se passa nos Estados Unidos, que vão à frente na tendência do eficientismo?

"Banks just can’t figure out what to do with their branches.

...

The efforts are proving tricky given that banks want customers to come to branches for moneymaking financial products such as loans or credit cards, but also have to serve the millions of Americans who still regularly make deposits and withdraw cash at the teller line.

...

Bank of America Corp. soon will begin converting about 9,000 tellers to “relationship bankers” who can direct customers to high-tech ATMs or show them how to deposit a check via smartphone.

...

Despite banks cutting costs sharply in recent years, as many as one-third of those branches remain unprofitable, says consulting firm Simon-Kucher & Partners.

...

“Nobody buys a home equity line of credit on impulse,” ... In some cases, the changes risk turning off customers.

...

Some firms are simply shuttering branches. Fifth Third Bancorp last month announced that it will close or sell 100 branches, or 8% of its offices. Like many of its peers, the Cincinnati-based bank also is expanding its use of employees who can handle a variety of functions."

Entretanto no Twitter, encontrei estes tweets de Esko Kilpi, bem em linha com a mensagem deste blogue (ler de baixo para cima):

Recordar "The Three Rules" de Raynor e Ahmed:

- Better before cheaper;

- Revenue before cost;

- There are no other rules

O que é que os bancos andam a fazer há anos?

.

A fugir da interacção e a fugir daquelas 3 regras.

.

Para terminar, este trecho retirado de "Home and Away" na revista "Health Club Management":

Quem não aposta no "cheaper" e no "cost", aposta na interacção, aposta na co-criação, aposta noutro mindset... eu diria, "Every visit customers have to make are an opportunity for interaction and co-creation"

.

Nunca esquecer, Golias pode apostar e ganhar com a automação porque está no seu ADN; contudo, David não tem qualquer vantagem em seguir esse caminho, tem muito mais a perder do que os euros que poupa.

Trechos 2 retirados de "

Is This a Coffee Shop or a Bank?"

%2006.21.jpeg)