Neste postal "

Confusões acerca da eficiência e da produtividade" comentei o artigo "

Should Your Business Be Less Productive?".

.

Agora, ao relê-lo, percebi que esqueci-me de comentar o lead:

"Many contemporary businesses are on a quest for productivity gains. They seek to maintain quality and quantity of output at ever-decreasing cost, yielding higher profitability. As advanced economies move more into the service sector, that means many managers devote a lot of attention to designing automated processes that reduce the need for people — typically their most expensive resource."

Este é o erro principal de quem quer aumentar a produtividade.

"They seek to maintain quality and quantity of output at ever-decreasing cost"

Aquele "mantendo a qualidade" afunila o campo de possibilidades

Rápido, o que é que é preciso para aumentar a produtividade, mantendo a qualidade e quantidade do que se produz?

.

É preciso cortar!

.

Sabem qual é o impacte dos cortes nas margens? Claro que sabem,

Marn e Rosiello e muitos outros mostraram-nos este gráfico:

Voltemos ao texto acima:

"that means many managers devote a lot of attention to designing automated processes that reduce the need for people — typically their most expensive resource"

Pessoas são um custo fixo... qual o efeito do corte de 1% nos custos fixos?

.

É só olhar para o gráfico.

.

Qual o problema daquela frase inicial?

.

É só olhar para o gráfico.

.

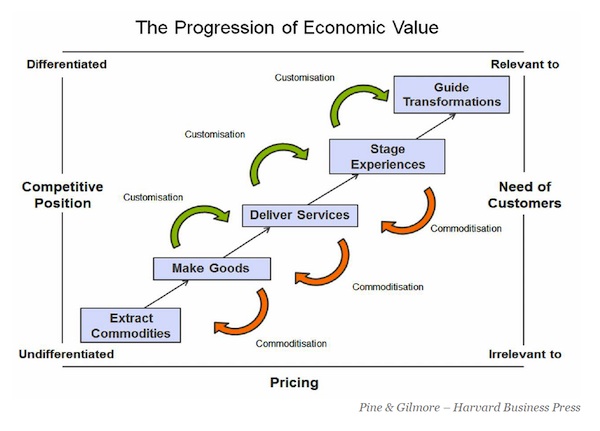

Gilmore e Pine criaram esta figura para ilustrar a evolução económica:

Aquela frase inicial foi esculpida na pedra no tempo em que só se transaccionavam commodities. Hoje, num tempo em que as experiências se impõem, a melhor forma de aumentar a produtividade passa por melhorar, por aperfeiçoar a experiência. Se falarmos numa lógica de produto, podemos dizer que o truque é alterar, melhorar, aperfeiçoar a qualidade.

.

Se o que oferecemos é diferente e melhor... pode ser vendido por um preço superior... qual o impacte desse aumento?

.

É só ver o gráfico acima.

.

Qual é o factor com maior efeito de alavanca?

%2006.21.jpeg)