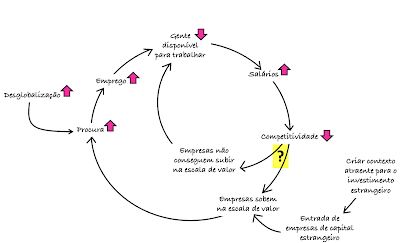

O fim da globalização (parte IV) + Parte I, parte II e parte III.

O autor prevê o colapso do comércio intercontinental por causa da ascenção da pirataria. Uma perspectiva interessante que nos obriga a pensar no que tomamos como garantido:

"Long-haul transport is what brings everything from areas of high supply to high demand, regardless of participant. For any product that is concentrated in terms of supply or demand, expect market collapse.

...

The Western Hemisphere is fine for foodstuffs and energy but will need to build out its manufacturing capacity for products as wildly varied as laptops and shoes. The German bloc’s manufacturing capacity is largely in-house, but the raw inputs that enable it to operate are wholly absent. The Japanese and Chinese are going to have to head out to secure food and energy and raw materials and markets. It’s a good thing that Japan likes to manufacture products where it sells them, and fields a potent long-reach navy. It’s a bad thing that most of China’s navy can’t make it past Vietnam, even in an era of peace

...

First and most obvious are the pirates. Any zone without a reasonably potent local naval force is one that is all but certain to host Somalia-style pirate harassment. Second and less obvious are the privateers, in essence pirates sponsored by an actual country to harass their competitors, and who have been granted rights to seek succor, fuel, and crew (and sell their *ahem* booty) in allied ports.

...

The third security concern isn’t likely to be constrained to the no-man’s-lands: state piracy. We’re moving into a world where the ability to import anything—whether it be iron ore or diesel fuel or fertilizer or wire or mufflers—will be sharply circumscribed.

...

Everything we’ve come to expect about transport since 1946 dies in this world. Bigger, slower, more specialized vessels are little more than tasty floating buffets for whatever privateer or pirate (state or otherwise) happens to be in the area. Larger vessels might maximize efficiency in a unified, low-threat world, but in a fractured, high-threat environment they also concentrate risk.

...

That’s a massive problem for German manufacturing, as many of its suppliers are from beyond the horizon and roughly half of its customers aren’t even in Europe."

Trechos retirados de "The End of the World is Just the Beginning" de Peter Zeihan.